Excerpts from analysts' reports.....

RHB Research sets 84-c target for Food Empire

RHB Research sets 84-c target for Food Empire

Packaging of Food Empire's top selling-product, MacCoffee, being printed in its packing plant in Jurong, Singapore. Food Empire has plants in Malaysia, Vietnam, Russia and Ukraine too. NextInsight file photoAnalysts: Melissa Yeap & Terence Wong, CFA

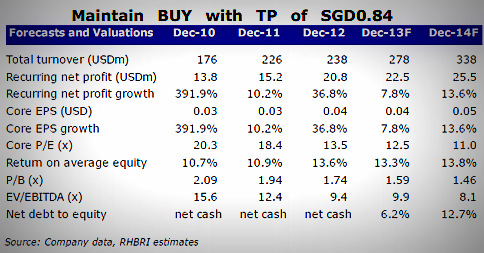

Packaging of Food Empire's top selling-product, MacCoffee, being printed in its packing plant in Jurong, Singapore. Food Empire has plants in Malaysia, Vietnam, Russia and Ukraine too. NextInsight file photoAnalysts: Melissa Yeap & Terence Wong, CFAWe recently hosted Food Empire for a roadshow in Singapore.

Among the key takeaways are: 1) Management has turned more bullish in terms of topline growth, 2) Backward integration plans are on track and should come on-stream in 3Q13.

While we raise our FY13/14 revenue growth projections to 17%/21%, our earnings remain largely unchanged as we take into account higher depreciation and start-up costs.

We continue to like the firm for its dominant position in Russia and Eastern Europe.

Reiterate BUY with an unchanged TP of SGD0.84.

This translates into 16x FY13F P/E vs Super Group which is trading at 26x.

Recent story: FOOD EMPIRE: US$21 m net profit in FY12, upstream projects taking shape

Lim & Tan Securities is latest research house to highlight value in GuocoLeisure

Out of the 8,280 rooms in UK that GuocoLeisure operates, 5,110 rooms are in London. The company operates under two hotel brands, namely, Guoman and Thistle. Photo: CompanyAt S$0.75, Guocoleisure trades at a 30% discount to its NAV of S$1.09.

Out of the 8,280 rooms in UK that GuocoLeisure operates, 5,110 rooms are in London. The company operates under two hotel brands, namely, Guoman and Thistle. Photo: CompanyAt S$0.75, Guocoleisure trades at a 30% discount to its NAV of S$1.09.

The company was at the centre of a failed privatisation exercise in 2005 with Malaysian tycoon Quek Leng Chan offering S$1.25 for its entire issued share capital.

Quek’s privatization attempt was blocked by 2 institutional shareholders then, but he has been steadily increasing his stake to close to 67% currently.

Quek had offered to take private Hong Kong listed Guoco Group in Dec 2012 at 0.7x price to book and Hong Leong Capital at 1x price to book in Jan 2013.

Both company share prices are currently above Quek’s takeover offers. The release of the IFA report by end Apr 2013 could well act as a re-rating catalyst for Guocoleisure.

Its valuations are also undemanding at 0.7x price to book,10x PE and 3% yield.

We believe the stock has speculative appeal but also note the stiff technical resistance around the 80 cents level which has been a key resistant level established since 2009.

Lim & Tan Securities is latest research house to highlight value in GuocoLeisure

Out of the 8,280 rooms in UK that GuocoLeisure operates, 5,110 rooms are in London. The company operates under two hotel brands, namely, Guoman and Thistle. Photo: CompanyAt S$0.75, Guocoleisure trades at a 30% discount to its NAV of S$1.09. The company was at the centre of a failed privatisation exercise in 2005 with Malaysian tycoon Quek Leng Chan offering S$1.25 for its entire issued share capital.

Quek’s privatization attempt was blocked by 2 institutional shareholders then, but he has been steadily increasing his stake to close to 67% currently.

Quek had offered to take private Hong Kong listed Guoco Group in Dec 2012 at 0.7x price to book and Hong Leong Capital at 1x price to book in Jan 2013.

Both company share prices are currently above Quek’s takeover offers. The release of the IFA report by end Apr 2013 could well act as a re-rating catalyst for Guocoleisure.

Its valuations are also undemanding at 0.7x price to book,10x PE and 3% yield.

We believe the stock has speculative appeal but also note the stiff technical resistance around the 80 cents level which has been a key resistant level established since 2009.

A successful break above this critical level would signal higher levels.

Recent articles:

Recent articles:

There's Deep Value in GUOCOLEISURE, says CIMB after company visit

HIAP HOE & GUOCOLEISURE: Catalysts for re-rating