IF A STOCK went IPO at 54 cents -- as Synear Food did - and recently traded at 13 cents, it’s a nasty fall indeed.

In the case of Synear Food, it’s been a nightmare many times over for investors who bought the stock when it was a market darling after its IPO in Aug 2006.

The stock had climbed to, and stabilised, above $1.50 throughout 2007.

After spiking up to nearly $2.50 in Oct 2007, it crashed during the Global Financial Crisis of 2008.

When the market recovered in 2009, somehow the pieces of Synear never quite came together again.

As a result, Synear is among the worst performing S-chips (or non-S-chips) still around today - ie, if we exclude those that have been suspended for accounting issues.

In absolute dollar terms, Synear has lost over S$3 billion in stock value in the last 4-5 years. That's massive value destruction indeed.

It is hard to imagine Synear as being one of China's largest producers of frozen food, including sweet and meat dumplings.

And it was an official supplier to the 2008 Beijing Summer Olympics?

In fact, the Synear brand has been voted as one of "China's Top 500 Most Valuable Brands" for seven consecutive years from 2004 to 2010.

What wonderful accolades -- but where are the glorious profits for investors?

The chart for its stock price says it all – the flattish line resembles the extremely dire condition of a hospitalized patient on a life-support machine.

The causes of Synear’s profit downtrend ranged widely, from high raw material prices to high labour costs to high advertising expenses, and what not.

And now a new problem has cropped up -- adverse publicity in 3Q concerning a batch of contaminated Synear products, which had a “significant negative impact on our revenue in 4Q2011.”

As a result, on 9 Jan, Synear said it expected to report a loss for 4Q.

Depending on how bad 4Q was, the stock's PE for FY2011 could be 13-15x.

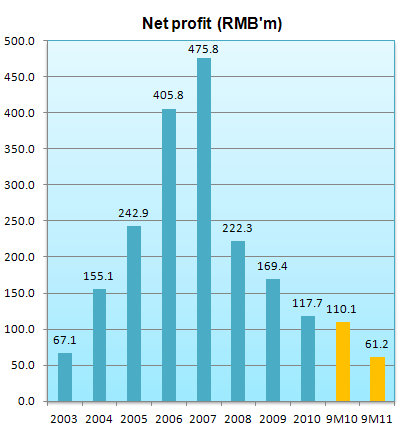

All the bad news makes it hard to believe that Synear once could do no wrong as its profit marched upwards relentlessly -- prior to IPO, of course (see chart).

At its peak in 2007, Synear had a market cap of S$3.4 billion. Today, it’s just S$179 million.

2007 happens to be the year Synear’s earnings peaked – at RMB475.8 million. It’s been sliding ever since, so what else could the stock do but slide too?

So it's not just about the market being averse to S-chips following a spate of cases of accounting fraud.

Like most S-chips, Synear did not stop raising funds through the issue of new shares after its IPO.

From 1.25 billion shares right after its IPO, the issued share capital now stands at 1.375 billion, or 10% more, after a single placement in 2007 (super timing by Synear but pity the placees!) at $1.85 cents a share.

Investors looking to its dividend yield for comfort will not find any: The dividend for FY2010 translates into a historical yield of merely 1.3%.

A positive of Synear is its net cash of 9 Singapore cents per share, which means cash accounts for about 70% of its market cap. It’s a dwindling amount, though, as Synear has significant capex for its new manufacturing and warehousing facilities.

If there is something to like about Synear currently, it is its net asset value of 47.23 cent a share (compared to its 13 cent stock price).

So it's trading at about a third of its NAV, which is one of the most heavily discounted stocks around, except for a handful trading at 0.2X price/book values.

Is this enough protection against further downside while one waits for the business profit to improve and, perhaps, lift its stock price?

Only time will tell. However, it could also turn out to be a value trap, if its business fundamentals do not regain their ability to whet investors' appetite. And, meanwhile, wouldn't investors be more ready to park their money in robust businesses whose stocks are already on the move in the nascent market rally?

IF you visit China supermarkets,you can see their presence.

Definately a much solid company compared to some of the S-chips.

Buyers beware

What is that intangible ?