Excerpts from latest analyst reports...

RS PLATOU: Cuts call on OOIL to 'neutral'

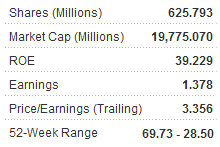

RS Platou Markets said it is reducing its recommendation on container shipper Orient Overseas International Ltd (HK: 816) to ‘neutral’ from ‘buy’ and cutting the target price to 44 hkd from 52.

“We don’t see a repeat of the credible operating performance by the company in 1H11 and expect 2H11 earnings to be a lot weaker in an increasingly challenging market. We expect OOIL to stay marginally profitable in 2H11 but reduced earnings and depressed overall sector sentiment will continue to weigh on the stock price,” RS Platou said.

RS Platou added that OOIL continues to be its favored container operating company with a proven record of maintaining higher operating margins, one of the lowest cost curves in the industry and strong management capabilities.

However, with fundamentals depressed, it will not remain unscathed.

“Given our negative sector view, freight rates declining further in the near term and absence of peak season in 2011, we reduce our earnings estimates for FY11 and FY12 net income by 35% and 54%, respectively.

“We do not expect sector recovery near term and believe any increase in freight rates can be brought upon only by collective actions of the carriers by supply side corrections in times of sharply faltering utilization levels.”

The company continues to enjoy a sound balance sheet and despite its capex and debt commitments, and RS Platou expects OOIL to comfortably tide over a period of reduced earnings.

See also: HONG KONG: ‘Zero Tolerance’ For Listco Irregularities

BOCOM: Remains 'positive' on PRC consmer sector

Bocom International said it is less bullish in 2012 on Mainland China's consumer sector, but still maintains a 'positive' outlook.

"We reiterate our 'outperform' call on the China/HK consumer sector as we move into 2012. That said, we are turning more cautious given the sector's reducing resilience due to the slower China consumption growth outlook amid rising macro headwinds.

"Moreover, we believe the increasing competitive threat and market consolidation will intensify the sector’s polarization effect."

Bocom said all this prompts the brokerage to have a more divided view on the different sub-segments in 2012.

Bocom's earnings forecasts in the consumer universe are now 2-28% below market consensus for FY12E and 5-36% below for FY13E, after its cut of 3%-8% for FY12E and 2%-8% for FY13E.

"We believe the stocks to look out for are those with stronger sales resilience, better visibility and proven track record of weathering market pressure. We favor department stores and ladies’ footwear the most in light of the sustainied solid growth momentum on healthy SSS growth and rising brand power, while we favor sportswear the least due to the mounting margin pressure and overexpansion concerns."

Bocom's top picks are Belle, Golden Eagle and Lifestyle while its least preferred stock is Boshiwa.

"Our other favorable stocks include Intime, Sa Sa, Le Saunda and Taifeng. We are cautious on Parkson, China Resources Enterprise, Anta and Daphne."

See also: VODONE: No.1 Mobile Gamer In China, Shares At 52-Wk Low... What Gives?