DMG says Sino Grandness’ result was surprise, ups target price to 50 cents.

Analysts: Tan Han Meng, CPA, CFA, Terence Wong, CFA

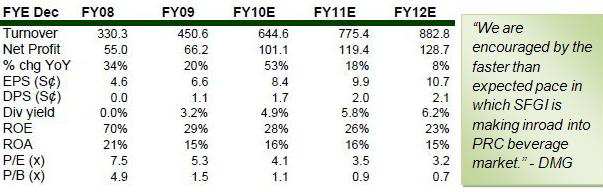

Sino Grandness Food Industry Group’s (SFGI) 1H10 results surprised on the upside on stronger-than-expected beverage revenue and gross margin, making up 23% and 29% (our estimates: 17% and 16%) of Group’s revenue and gross profit respectively.

This prompted us to revise our

a) EPS forecast upwards by 8%, and

b) target multiple to 6x FY10F P/E (previous: 5x) as its beverage business model is taking shape earlier than anticipated. Our new derived TP of S$0.50 (previous: S$0.40) represents 45% upside potential. Maintain BUY.

1H10 exceeds expectations. Net profit was up 86% to RMB41m as revenue doubled to RMB244m with strong growth across both canned and beverage segments. Gross margin was a lower 29% (1H09: 33%) due to weakness from canned division, which was partially mitigated by strong domestic beverage performance. Better costs control kept net margin stable at 17%. 1H10 revenue and net profit made up 41% and 44% of our FY10F estimates.

Stable canned vegetable and fruit growth. Revenue from canned division grew 55% to RMB186m on higher customers’ orders. Affected by lower ASP as a result of market development efforts in both existing (e.g. Europe and Mexico) and new (e.g. Australia) markets, gross margin is estimated to have contracted 6ppt to 27%.

Maiden beverage contribution. Beverage surprised on both revenue and gross margin. At RMB57m, beverage made up 56% of our full-year revenue estimates. Gross margin of 36% was also higher than 26% achieved last year.

Balance sheet to improve in 2H. Cash balance decreased RMB110m to RMB37m due to 1) RMB62m bank and notes repayment, 2) RMB14m dividend paid, and 3) RMB42m capital expenditure. Overseas shipments in seasonally stronger 2H will likely improve cash position.

Re-rating catalyst: beverage business model taking shape. We are encouraged by the faster than expected pace in which SFGI is making inroad into PRC beverage market. The company recently announced the signing of 16 distributorship agreements across seven provinces for its new Fruit&Veg beverage, after noting encouraging response since its launch in Mar. Revenue from the new series is estimated to be around RMB30m (our estimate: nil) in 1H. These positive developments resulted in a re-rating of our target multiple to 6x FY10F P/E (previous: 5x).

Recent story: SINO GRANDNESS: Top exporter of canned asparagus, long beans, mushrooms

CIMB cheers JADASON’S 2Q result, maintains ‘buy’ rating

Analyst: Jonathan Ng

• 2Q10 results in line; maintain BUY. Jadason’s 2Q10 results were sterling, as expected. What surprised was an interim dividend of 0.2ct.

We leave our FY10-12 numbers intact, and see the company as a good proxy for the recovery in the tech sector. Our unchanged target price of S$0.125 conservatively pegs Jadason at 6x CY11 P/E – the lower end of its 5-year trading band of 4-16x.

Fung Chi Wai, CEO, Jadason. Photo by Leong Chan Teik

Fung Chi Wai, CEO, Jadason. Photo by Leong Chan Teik

We see catalysts from:

1) continuous strong quarterly results;

2) further improvements in its balance sheet; and

3) possible upside surprises in full-year dividend payment.

What we like:

• Strong recovery in the distribution business and healthy growth for manufacturing services

• Turnaround of distribution business in 2Q on the back of higher sales and further margin expansion for manufacturing services on a better sales mix

• Another quarter of good cash flow, ending in a net cash position in 2Q10, two quarters ahead of our expectations

• Positive surprises in dividend payment. An interim dividend of 0.2ct was declared, translating into a decent yield of 2%.

What we dislike:

• Slower-than-expected contributions from its new printing equipment business as the group is still fine-tuning the machine.

Outlook: Still busy in early 3Q

• As highlighted in our note dated 26 Jul, Jadason is still enjoying good loading for drilling services and mass lamination. As a result, it has been more selective in customers and projects, focusing on jobs with better margins to optimise returns.

• With the improved macro environment, Jadason plans to add capacity gradually for its drilling and mass lamination business by year-end.

• Order book for the equipment distribution business remained healthy at US$20m at end-June. Jadason should book another quarter of good growth.