A reader, MOSBY, last night highlighted in NextInsight’s forum an analyst report on Rokko. Excerpts are presented here from the July 23 report by Lim & Tan Securities.

At yesterday’s analysts presentation, management was upbeat about prospects, citing their major customer Texas Instruments (accounts for about 50% of their business) robust outlook and their 50% rise in order books since early this year to $15mln currently.

Our independent check on Texas Instrument shows that their book to bill ratio of 1.07x suggests that their orders are coming in more than they can deliver which was why they recently upped their capex budget from US$900mln to US$1.2bln, way above last year’s US$500mln.

* After reporting an all time record sales and profits for 2Q ’10, management is guiding for even stronger 3Q ‘10 (+10%) as their customers prepare for back to school, Christmas and Chinese New Year sales over the next few months.

* Another major customer the world’s 4th largest wafer foundry SMIC is also raising its budgeted capex to double last year’s level at US$800mln due to its book to bill ratio of above 1x. This is expected to help its revenues double over the next 2 years.

* STATS Chippac a top 5 customer of Rokko does not provide guidance nor update the investor community, but their 1Q ‘10 sales rose 76% yoy to a record $388mln and upped their capex by 10 folds from $9.5mln to$99.5mln as their utilization rate is running close to max and orders continue to remain strong.

* Other bellweather chip players such as Intel, AMD, TSMC and UMC are also guiding for similarly upbeat prospects.

* The above upbeat prognosis from major chip producers and major customers of Rokko ties in with independent research body Semiconductor Equipment and Materials International which is predicting for the industry to rise 65% this year to US$2.31bln.

* The company’s metal stamping division is expected to benefit from the robust PC sector (expected to rise 20%this year) as well as new and higher margin chemical plating business.

* Rokko is preparing for further growth and have acquired a 3 storey factory with built-in area of 17,130 sqf to expand their equipment manufacturing business. The company will also be starting a new factory in Malaysia and China later this year to take on new business opportunities. (The company recently placed out 15mln new shares at 14 cents each to help fund part of their capex plans)

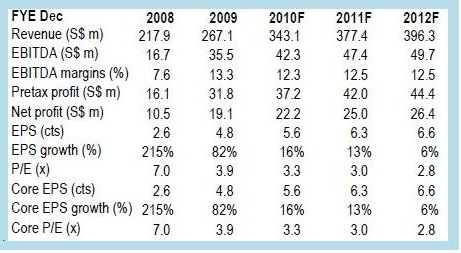

* Management has recently guided for 1H ‘10 profit before tax of $3-3.5mln and profit after tax of $2.5mln-3mln. Based on their robust order books, 2H ‘10 is expected to be similar or slightly stronger.

* At 4-5x forward PE, its valuation is undemanding relative to sector peers such as MIT and Micro-Mechanic’s 9-12x average and based on management’s 30% payout ratio, yield is 6-7%. Maintain BUY.

Recent story: NRA CAPITAL's 9 best tech picks

CIMB sets 100% upside for ACTION ASIA stock now trading at 3.3X this year's forecast earnings

Analyst: Jonathan Ng

Reiterate BUY. Another set of sterling results came from Action in 2Q10, with sales and net profit leaping 77% and 30% yoy, respectively. This marked its 10th consecutive quarter of double-digit earnings growth.

We believe the momentum will continue in 3Q (typically the busiest for consumer electronics products), driven by its continuous efforts to deliver innovative consumer lifestyle entertainment products. We leave our FY10-12 profit forecasts unchanged.

Action remains attractive, at 3x CY11 P/E and below its CY10 book value. Our target price remains S$0.40, offering more than 100% upside. This pegs Action at slightly below 6x CY11 P/E.

* Solid topline growth, reflecting its success with Philips. Action shipped close to 1.5m DVD players (mostly portable type) in 2Q, up from about 1m in 1Q10.

• 10th consecutive quarter of double-digit yoy profit growth. Bottom line would have been stronger, excluding S$278k for assets written off.

• Drop in gross margins and spike in staff costs. We believe the margin decline was the result of its product mix (increased volume of standalone DVD players) and higher raw material costs, while higher staff costs were due to more manpower required to support the higher volume.

• Extended cash cycle days as longer A/R and inventory days were not offset by longer AP days. The longer A/R days were due to extended credit terms for its major customer from 75 days to 90. This resulted innegative free cash flow and marginal net debt in the quarter. Action is working with its suppliers to lengthen its credit terms.

Positives:

• Order momentum remains robust in the seasonally strongest 3Q withno signs of a slowdown from key customer. However, order visibility for 4Q remains cloudy at this moment. This is not surprising as we have assumed peak earnings in 3Q and a slowdown in 4Q.

• Raw material availability has improved, and there is more room forprice negotiations in 3Q. This could ameliorate ongoing pricing pressure.

Negatives:

• Action is affected by higher labour costs, which jumped by 20% in June. It is trying to rope in its major customers to help in the rising costs. It is also trying to improve productivity to counter the higher wages.

• More aggressive bidding by some domestic consumer electronics makers, which is affecting Action in terms of pricing.

Recent story from the company's AGM: ACTION ASIA: On dividend cut, soaring growth prospects, etc

Nomura Singapore highlights positive surprise for BIOSENSORS, reiterates buy call

Analysts: Lim Jit Soon, CFA, and Tsai Yuan Yiu

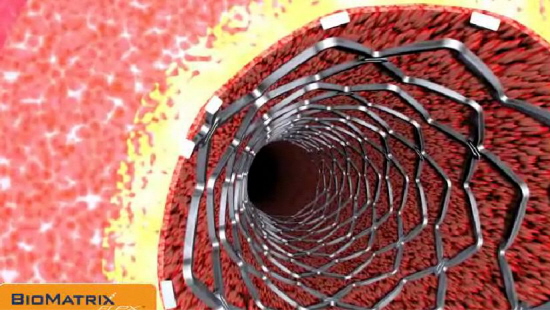

Event. According to its press release dated July 29 2010, Devax Inc announced that the company has recevied CE Mark for its AXXESS Biolimus A9 Eluting Bifurcation Stent System, allowing the company to initiate sales in the EU and other CE markets (mainly Asia ex-Japan, China and Latin America).

Licensing agreement with BIG. Under a licensing agreement dated December 2003, Biosensors is entitled to: i) receive royalties, including an annual minimum royalty, based on an undisclosed percentage of AXXESS revenue and ii) provide stent-coating services to Devax at a premium above cost.

How big is the "bifurcation" market? According to In Vivo, bifurcation disease (vascular disease located at the division of one artery into two) remains one of the largest unmet clinical needs in interventional cardiology, affecting roughly 20% of patients who undergo PCI; the potential market size is esimated to be US$1.3bn worldwide. Based on our preliminary research, AXXESS is one of the few pioneers in this technology with a CE mark, and none of the Big Fours has been successful in commercializing a similar product so far.

More possibilities going forward? Biosensors new CEO Jeff Jump's key strategy going forward is to broaden its product range to better leverage on its existing sales/R&D/manufacturing infrastructure, via both acquisitions and internal R&D. Therefore we think there are more possibilities to this partnership, which could potentially involve a distributorship. In this regard, we believe Biosensors would be able to provide speed-to-market by sharing its knowledge base on reiumbursement approval process in key markets such as France and access to its existing direct sales infrastructure.

Potential royalties not in our estimates. We have not factored in the potential royalty stream and stent-coating revenue from Devax given the lack of visibility over the approval timeline previously and the undisclosed royalty formula. While the cashflow potential is unlikely to match Terumo's licensing agreement, we think this reaffirms our investment thesis that there is significant value to be unlocked at Biosensors. Reiterate BUY.

Recent story: BIOSENSORS, COMTEC SOLAR: What analysts say now....