The effective all-in interest rate on the new loan will be 6.6% (although the cash interest cost is circa 4.9-5.4% by JP Morgan estimates), once all fees and loan premia are accounted for.

JP Morgan (Overweight) said: “The near-term going concern issues for this REIT have now been all but removed. All except one of the trust’s properties have been charged as collateral for loans which have standard debt covenants. We lower our FY09-10 DPU forecasts by 17-19% to take into account the higher costs of debt, and also to make some provision for unanticipated vacancies.

Key downside risks are on operational issues and stock illiquidity:

CIT’s portfolio is made up of relatively long-term leases, but the economic downturn raises the prospect of revenue shocks from sudden, unanticipated vacancies or rental adjustments to sustain occupancy rates.The stock’s FY09 distribution yield is 22% on our estimates, but we fear the stock will likely remain illiquid for now with an attendant hike in its costs of equity capital.

End-Dec-09 price target lowered to S$0.38/unit (S$0.77 previously):

We lower our DDM-based end-Dec-09 price target to S$0.38/unit, predicated on an equity discount rate of 13.88%. Critical stock milestones may well come externally as the S-REIT sector negotiates a round of debt re-financing, balance sheet restructuring, and equity recapitalization.

*****

Nomura Research (Neutral) said: “The wider implication for S-REITs on the whole following this announcement is likely to be positive, and should help to allay much of the concern over refinancing, since Cambridge, one of the smaller S-REITs with no sponsor, has proven its ability to secure refinancing.

More importantly, while the eventual cost of debt is higher than we were expecting, it is still far lower than the market was pricing in prior to the announcement, on our estimates.

While the eventual cost is higher than our expectation, it is far lower than the market was pricing in prior to the announcement. This development should allay much of the refinancing concern over the S-REITs.

Maintain ‘neutral’ rating.

*****

UOB Kayhian (Buy) said: “We have revised our forecast to factor in the higher cost of borrowings. We

expect occupancy to taper off to a lower 93% by 2Q09, compared to our previous assumption of 96%. We cut our FY09 DPU forecast by 17.7% from 5.1 cents to 4.2 cents.

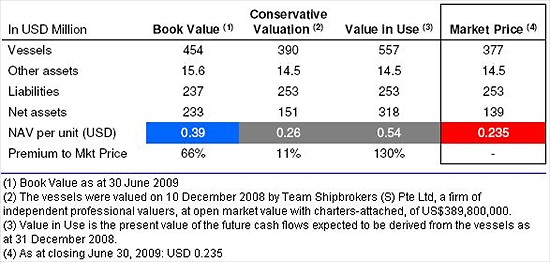

Recent correction in CIT’s share price is overblown. CIT provides FY09 distribution yield of 21.5% and trades at 74.3% discount to NAV/share of S$0.76. Its share price has also corrected 80.1% from the peak of S$0.98 in mid-07 and is trading at 71.3% below the price of S$0.68 during the initial public offering in Jul 06.

Reiterate BUY with new target price of S$0.62, based on a two-stage dividend discount model (required rate of return: 9.0%, growth: 2.5%).

Recent story: CAMBRIDGE REIT: Fair value is $1 (according to sexy VJC girl)