|

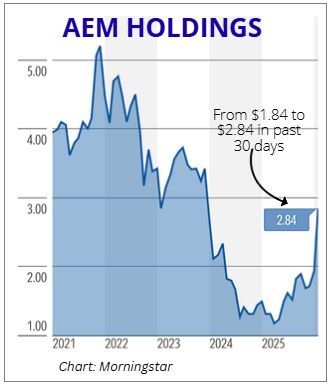

For the past few years, AEM Holdings, a semiconductor testing company, went through a grueling period that smashed its stock price. |

|

Financial Highlights (S$’000) |

FY25 |

FY24 |

Change (%) |

|

Revenue |

399,338 |

380,410 |

5.0 |

|

Profit before tax (PBT) |

21,330 |

14,071 |

51.6 |

|

PBT margin |

5.3% |

3.7% |

1.6 ppts |

|

Net profit |

17,148 |

11,606 |

47.8 |

|

Net profit margin |

4.3% |

3.1% |

1.2 ppts |

Buoyed by a substantial Free Cash Flow of S$112.1M in FY25, AEM signaled confidence in its turnaround by resuming its dividend payments.

The stock has rebounded sharply on these FY25 results, with analysts aggressively raising their target prices.

DBS analyst Amanda Tan, who was early in pivoting to an optimistic call on AEM, notes, "Our non-consensus BUY call has played out well, with the stock delivering close to 80% gains since our upgrade in Nov-24".

Why the new wave of optimism? Analysts point to several key drivers:

1. The AI/HPC Boom and a New Anchor Customer

The most significant catalyst is the rapid ramp-up of AEM's second Artificial Intelligence and High-Performance Computing (AI/HPC) customer, which is projected to overtake AEM's legacy customer (ie Intel Corp) to become the group's largest client in FY26.

"AEM is also excited by the surge in CPU demand, which is already translating into increased orders from its long-standing HPC customer and should directly benefit AEM in the near term. AEM is now extending this momentum into memory test, with customer validation on track for production in late-26." "AEM is also excited by the surge in CPU demand, which is already translating into increased orders from its long-standing HPC customer and should directly benefit AEM in the near term. AEM is now extending this momentum into memory test, with customer validation on track for production in late-26."-- John Cheong, UOB KH analyst |

Validating this shift, UOB Kay Hian analyst John Cheong states, "The rapid ramp of AEM’s strategic AI/HPC customer’s business over the past year validates its leadership in advanced logic test and positions AEM at the forefront of structural semiconductor growth".

2. Exceptionally Strong FY26 Guidance

AEM provided strong revenue guidance of S$460-S$510 million for FY26, anchored by multi-year AI demand.

Reflecting the market's enthusiasm, Maybank analyst Jarick Seet explains, "We believe the ramp-up we have been waiting for is finally here with the new revenue guidance for FY26E".

3. Expanding Margins and Earnings Upcycle

The Test Cell Solutions (TCS) segment, which yields higher margins than the other core segment -- contract manufacturing -- grew 9% year-on-year.

The anticipated surge in TCS orders is expected to drive a broader recovery in net margins and operating leverage.

Highlighting this trajectory, CGS International analyst William Tng projects, "As AEM moves into its next 3-year (FY26-28F) earnings upcycle, we see a potential valuation uplift to +3 s.d. P/E multiple of 17.4x, supported by EQDP buying demand".

4. Successful Customer Diversification

Beyond its new AI/HPC anchor, AEM is successfully pushing into the memory testing market.

Equipment evaluation with a leading tier-1 memory customer is well on track, with production units slated for delivery in late FY26 ahead of a full production ramp in FY27.

Here is how analysts have revised their target prices in response to AEM's stellar update on its outlook:

Ultimately, AEM has survived its darkest days and emerged stronger with innovations in chip testing. Positioned at the forefront of semiconductor growth, analysts believe the company is poised to ride the ongoing multi-year AI supercycle with a broader base of core customers. |

→ See the reports: CGS, UOB Kay Hian, DBS Group, Maybank.

→ See the reports: CGS, UOB Kay Hian, DBS Group, Maybank.