Excerpts from CGS-CIMB report

Analysts: William Tng, CFA & Izabella Tan

ISDN Holdings Ltd

■ ISDN announced that its first mini hydropower plant has achieved COD (commercial operation date) and expects meaningful contributions from this plant in FY23F.

■ With its hydropower business contributing over FY23-24F and resumption of activities in China, we upgrade ISDN to an Add as we also rollover to FY24F. |

|||||

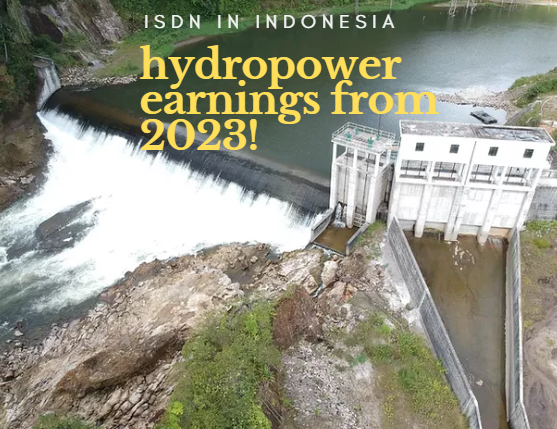

Lau Biang 1 (LB1) receives COD

ISDN announced that its first mini hydropower plant, LB1 (10MW capacity), has received the commercial operation date (COD) as of 31 Dec 2022.

| "Anggoci (10MW capacity) and Sisira (4.6MW capacity) were successfully commissioned in Sep 2021. Anggoci and Sisira faced delays in obtaining CODs due to regulatory changes. We are hopeful that these two plants could finally achieve COD within 1H23F." |

In its public filing, ISDN also commented that it expects meaningful contributions from this plant for FY23F.

The company has also revealed that more details will be disclosed through an investor briefing in due course. To recap, ISDN currently has a portfolio of three mini hydropower plants in North Sumatra, Indonesia.

Anggoci (10MW capacity) and Sisira (4.6MW capacity) were successfully commissioned in Sep 2021. Anggoci and Sisira faced delays in obtaining CODs due to regulatory changes. We are hopeful that these two plants could finally achieve COD within 1H23F.

Covid-19 disruptions tailing off

In China, there are two positive developments for ISDN. First, China is now shifting its focus to the economy after three years of prioritising the management of the Covid-19 pandemic.

Second, starting 8 Jan 2023, China will also downgrade Covid-19 to a Class B infection and largely eliminate quarantine and movement control measures.

This will allow further resumption of business activities in China though there will be an impact from the initial wave of infections as restrictions are dismantled which could affect activities. Hence, operationally we expect sequential improvement for ISDN starting from 2Q23F.

Rolling over to FY24F

Pending updates from ISDN through a planned investor briefing (date has not been fixed) as publicly announced by the company, we interpret meaningful contribution to mean 5-10% of net profit and assume that Lau Biang 1 could add an incremental 10% to our FY23-24F net profit forecasts.

Hence, our FY23-24F EPS forecasts are raised by 11.1%.

William Tng, CFA.Rolling over to FY24F (previously FY23F), our TP increases to S$0.55 based on 8.9x (5-year average P/E multiple). William Tng, CFA.Rolling over to FY24F (previously FY23F), our TP increases to S$0.55 based on 8.9x (5-year average P/E multiple).Previously the 5-year average P/E multiple was 8.6x.  Izabella TanWe upgrade ISDN to an Add as its hydropower earnings commence contribution to its bottomline and business prospects improve from 2Q23F. Izabella TanWe upgrade ISDN to an Add as its hydropower earnings commence contribution to its bottomline and business prospects improve from 2Q23F.Re-rating catalyst is higher-then-expected net profit contribution to ISDN from its hydropower business segment. |

Downside risks are the emergence of new Covid-19 strains which could bring back lockdowns, weak customer demand as the global economy slows and the possibility of bad debts as economic conditions worsens.

Full report here.