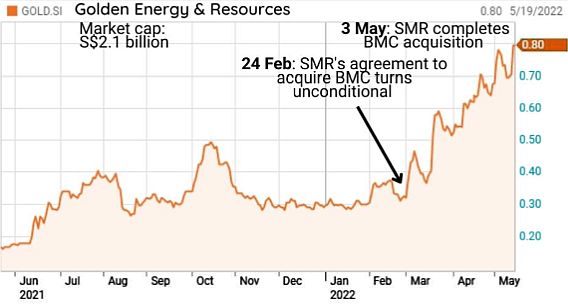

The share price of Singapore-listed Golden Energy & Resources has surged 142% to date this year. Aside from handsome profits from its Indonesian thermal coal mines, a key catalyst is its 64%-owned ASX-listed subsidiary, Stanmore Resources, acquiring a large coking coal asset in Australia -- at a bargain US$1.35 billion.

Celebrating the completion of BMC acquisition (L-R): Fuganto Widjaja (Executive Chairman, GEAR), Tim Peirce (M Resources), Shane Young (Stanmore CFO), Mark Zhou (Executive Director/Chief Investment Officer, GEAR), Dwi Prasetyo Suseno (CEO, GEAR), Marcelo Matos (Stanmore CEO).

Celebrating the completion of BMC acquisition (L-R): Fuganto Widjaja (Executive Chairman, GEAR), Tim Peirce (M Resources), Shane Young (Stanmore CFO), Mark Zhou (Executive Director/Chief Investment Officer, GEAR), Dwi Prasetyo Suseno (CEO, GEAR), Marcelo Matos (Stanmore CEO).

The analyst report below explains the prospects of Stanmore.

Excerpts from Morgans report

Analyst: Tom SARTOR

| Transformational met coal leverage The acquisition of BMC (80%) transforms Stanmore Resources’ operating scale, improves its risk profile and significantly improves its equity appeal.

Smooth BMC integration would also assist SMR to position for other coal sector divestments, delivering further potential value accretion. We initiate coverage with an Add rating and a $3.80ps target price, noting materially higher capital upside versus peers. |

||||

Transformation into a globally significant met coal player

▪ BMC acquisition: BMC lifts SMR’s metallurgical coal production to ~10.7Mtpa (#7 globally), with second-quartile costs driving significant cashflow leverage to good volumes over long mine lives. Larger established assets bring embedded revenue and cost opportunities and lower portfolio risk.

SMR also emerges with a more investible register.

▪ Rapid de-leveraging: We estimate SMR held ~US$680m in net debt on the May 2 handover assuming near fully drawn acquisition facilities (~US$825m gross debt, ~US$145m cash).

Our base case price forecasts support a CY22 EBITDA of ~US$1.4bn at ~60% margins, a 12-month BMC payback (EBITDA basis) and a net cash position in early 2023 including full debt service/ sweeps but pre dividends.

▪ Dividend upside: SMR’s CY22 dividend paying potential does sit behind its peers but improves rapidly post de-gearing.

Assuming no M&A and pre dividends, we forecast accumulation of ~US$525m/A$0.82ps of net cash by end CY23 (Bull case: ~US$744m/ A$1.16ps) available for capital management and/or M&A.

▪ Unique growth platform: SMR looks well positioned for further coal divestments via: 1) a strengthening balance sheet; 2) aligned major shareholders (assertive, liquid); and 3) northern Bowen Basin synergies.

Mitsui’s 20% BMC stake and BHP’s 50% stake in Daunia (~4Mtpa met neighbouring Poitrel) are obvious targets offering potential accretion. We note smooth BMC integration would assist in acquiring similar large assets.

▪ SMR is too important to mis-handle: Market unfamiliarity with GEAR (64% of SMR) is a potential impediment.

On page 9 we explain our comfort in the alignment of interests between minority shareholders and GEAR, but we do note SMR suits assertive, growth-oriented investors with a higher risk appetite.

Forecast and valuation

▪ Our SMR modelling methodology (from page 5) is consistent with our approach to CRN/ WHC/NHC and we test key comps/sensitivities via four coal price scenarios.

| Investment view ▪ We are increasingly of the view that stronger-than-expected met coal pricing will persist through CY22 on solid demand ex-China, coupled with very tight supply and exacerbated by disruption to Russian exports. The BMC acquisition has timed perfectly against this and provides a strong financial and strategic platform from which to grow, or failing that, release significant dividends.  A dragline bucket: A large form of excavator which can move overburden at much more economical rates. A dragline bucket: A large form of excavator which can move overburden at much more economical rates.▪ SMR offers 48-102% upside to our base/bullish NPV scenarios, respectively (Coronado: 25-57%). Our $3.80ps target price is set at an 80/20 blend of our base/bullish NPV scenarios to reflect upside risk to our coal price forecasts. ▪ We’re attracted to: 1) SMR’s compelling NPV discount; 2) superior upside leverage to higher coal prices; 3) scope for better-than-expected BMC cost-out initiatives; 4) further M&A optionality; 5) dividend upside; 6) ability to fully frank dividends. |

Price catalysts

▪ Rapid familiarisation, de-gearing and recognition of capital/dividend upside.

▪ Sector asset divestments (possibly 2HCY22).

Risks

▪ BMC integration, influencing achieved sales and costs.

▪ Macro-economic sensitivity (global GDP, steel) and ESG forces.

▪ Register turnover (majority of ~30% free float @ A$1.10ps).

Full report here