Kingsley Lucas Lim (photo) contributed this article to NextInsight. He had originally published it on his site, The Holy Financier.

Kingsley Lucas Lim (photo) contributed this article to NextInsight. He had originally published it on his site, The Holy Financier.

| Challenger Technologies, Singapore’s very own homegrown IT retailer, has a store footprint of 38-40 stores, the last I checked. If you look back on Challenger's history, it’s not too hard to figure out that delisting was an option that its promoters could take in the process of realizing value for themselves. I’m going to highlight some of the details and the signs that were evident in the financials of Challenger Technologies. In essence, the market has completely ignored what management of the company had done over the years to improve the business. As I have mentioned before, a lot of small caps have been taking a beating. |

"Terrific job growing Challenger Technologies"

The business of Challenger Technologies is one that is not too difficult to understand. It is simply an IT retailer founded in 1982. With a history that stretched far beyond the dot com bubble and the Asian Financial Crisis, the management had done a terrific job, in my opinion, of growing the business.

|

Year |

2003 |

2009 |

2017 |

|

Revenue (M) |

$67.3 |

$191.6 |

$320.6 |

|

Pre-Tax Profit (M) |

$4 |

$13.7 |

$19 |

|

Gross Margin (%) |

17.9 |

21.97 |

21.12 |

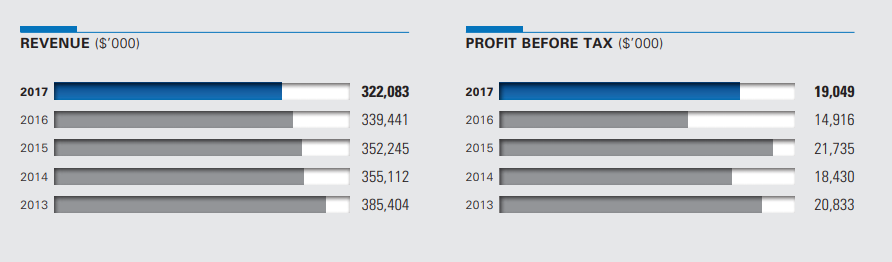

Just to give you a sense of that, the revenue was $67.3 million in FY 2003 and in that same year, it attained a pre-tax profit of just $4 million. In 2009, it attained revenue of $191.6 million and pre-tax profit of $13.7 million.

Even in such bad times, Challenger managed to churn out extremely good profits and cash flows. In 2017, Challenger Technologies had $320.6 million in revenue and and pre-tax profit of $19 million.

A table summarises the growth of Challenger Technologies. And if I may add, it looks pretty impressive.

Now of course, I am selective on the information here but it sure gives one a general overview of how the company had done under drastic economic conditions during the dot com bubble and the the subprime financial crisis. These “stress” years may highlight the durability of the business.

|

Year |

2013 |

2014 |

2015 |

2016 |

2017 |

|

ROE (%) |

30.78 |

23.38 |

25.65 |

15.85 |

19.63 |

Challenger Technologies currently has $61 million cash and no debt. It trades at an undemanding PE ratio excluding cash of 8.14 with stellar return on equity of between 19% and 30% over the last 5 years.

Its Enterprise Value to EBITDA is about 4 which is really cheap and Price to Free Cash Flow is around 7.5. These levels are completely undemanding and begs the question – Why is Challenger Technologies trading at such undemanding levels? What is the problem with Challenger Technologies?

5 Year Highlights Of Challenger Technologies

Looking at the 5 years results of Challenger, it seems that one of the reasons for its undemanding valuations is investor concerns over its growth. The last few years had seen a change in the landscape and the retail environment had gotten increasingly tougher. With the rise of e-commerce, Challenger had to find a way to reinvent itself and it did so by introducing Hachi.tech, its own online marketplace. The idea was to capture growth from the online audience as well.

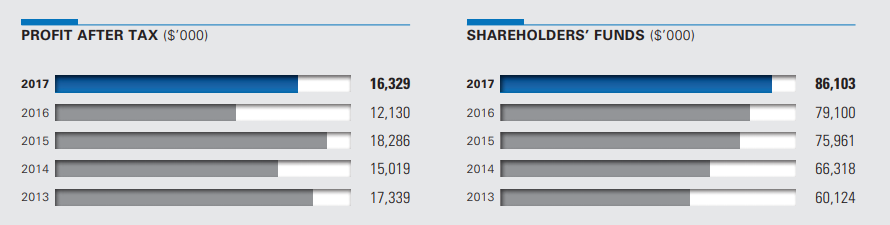

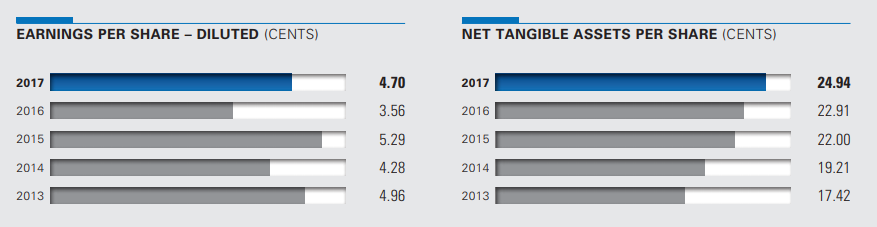

However, looking at the net profit numbers, it seems that year to year growth has been nearly non-existent at times. As such, there are no clear “uptrends” which the markets tend to favour. Another reason of course is the much talked about poor liquidity in Singapore’s stock markets. But I believe that to be a temporary situation and liquidity will eventually come back. Challenger’s operations remain profitable and you can discern that for yourself with its increasing net tangible assets over the years

Leverage Capacity

Ignoring all growth concerns for now, we look towards Challenger’s cash flow abilities. The company is enormously cash generative and has not raised funds from the public markets for 8 years.  Challenger Technologies CEO Loo Leong Thye. The average EBITDA/share is $0.13 for the last 5 years and if you think about some of the buyouts that have been occurring at EV/EBITDA multiples of 10 times with about 6 times of net debt to EBITDA employed, which is incidentally incredibly rich in my opinion, it is not too hard to fathom that 4 to 6 times EBITDA of debt can be placed on the company’s debt free balance sheet.

Challenger Technologies CEO Loo Leong Thye. The average EBITDA/share is $0.13 for the last 5 years and if you think about some of the buyouts that have been occurring at EV/EBITDA multiples of 10 times with about 6 times of net debt to EBITDA employed, which is incidentally incredibly rich in my opinion, it is not too hard to fathom that 4 to 6 times EBITDA of debt can be placed on the company’s debt free balance sheet.

That means that the company has an approximate debt capacity of $0.52 to $0.78 per share. Now, even with the offer to delist, the company trades at just $0.56 per share which is around or less than the debt capacity of the company. We are not talking about a scenario where a company is taken private at 10 times EBITDA.

We are talking about a company that is being taken private at slightly more than 4 times EBITDA. And I have to say that that is extremely cheap.

How is that even possible? Yes it is, in our extremely inefficient equity markets. But think about it this way: Even with $269 million in debt based on a debt capacity that is 6 times EBITDA, we are looking at $16 million in interest expenses which can be sufficiently covered by the company’s operating income of $40 million.

So as a shareholder, you stand to gain 2.69 million of value for every $1.93 million of share that you own in the case of a recapitalisation. That is a pretty decent deal if you ask me.

But that aside, can you imagine how ludicrous it would be if you went to a pawn shop and pawned your gold worth $1000 and received $1500 in return. Or just imagine this scenario where the house you would like to purchase is valued in the open market at $2 million but your bankers are willing to lend you $3 million for it? This usually never happens in real life. But in the equity markets, it does.

From a banker's point of view, if a bank assesses that it is willing to lend you $200 million to $300 million based on your business and the ability of the cash flows in the business to pay off its interest and debt, then wouldn’t it make sense that a debt free company with $200 million to $300 million should be worth at least its debt capacity, and perhaps even more with some financial engineering ?

Hence, the enterprise value of a company cannot be worth less than the comfortable amount of debt that it can service. That is purely commonsensical if you ask me.

Enter Dymon Asia Private Equity

So we all know that the company is undervalued and at the very least, I have painted it as such. You can choose to disagree with me of course. But the fact of the matter is that Challenger Technologies founding family and managers of the Loo family and Dymon Asia Private Equity have teamed up to make an offer to delist the company at a share price of $0.56.

|

|

Again, looking at the numbers above, it is quite a no brainer in my opinion. 56 cents is roughly 4 times EBITDA and the deal is most certainly one that will displace minority shareholders and squeeze them out.

The narrative from management is that they are facing a tough retail environment and are unlikely to give dividends in the years to come. I humbly beg to differ on this point. They will be able to give dividends for years to come.

E-commerce will change retail but there is also an adaptation phase for companies such as Challenger Technologies. They still have distribution relationships with their suppliers and manage their sales and inventory in a satisfactory way. It is not something that can be replicated immediately. And furthermore, Challenger still has the option to sell their inventory online, leveraging off the relationships with suppliers which they have built over decades.

So the deal that Dymon Asia has made is a purely commonsensical one. It made sense from so many different angles for the eventual private owners. The founding family owns about 78.64% of the common stock outstanding and Dymon will come in and inject the rest for the offer, which is worth about $41 million., nearly 10% of the Dymon Asia PE Fund II’s coffers of $450 million. That is what I believe anyway. I have to add that I am not privy to the details of the deal. This is calculated speculation on my part.

While minority investors have been lamenting the low ball offer price, in a capitalist society such as ours, it is a situation where “who dares wins”. Dymon Asia has stepped up to the plate and in a sense acted as an activist for themselves and the founding family. There is a lot of opportunities for activism in Singapore’s markets and that is another article for another day. I do have some ideas on activism though.

Anyway, this is what I see going forward. The business will be private for a few years at least. Since the acquisition or offer is not reported to be funded by debt, the company can be relisted at some 8 – 12 times EBITDA when the economy looks rosy again. This is at the discretion of the private owners, Dymon Asia and The Loo family. Another option is that the Challenger Technologies can be relisted in Hong Kong where the valuations are higher and the markets are more liquid.