OIL PRICES holding above US$100 a barrel this year has been keeping demand for oil exploration and production robust.

For Technics Oil & Gas, a market leader in Asia for integrating gas compression systems used in floating production, storage and offloading (FPSO) vessels, firm oil prices have translated into good profits, enabling the company to pay generous dividends over the past 2 years.

“Gas compression is critical to the function of the FPSO, like the heart in a human body”, said managing director Robin Ting at its results briefing yesterday.

In an FPSO, oil and gas received from its well-stream needs to be separated, and gas released from crude oil is routed via a gas compression unit for treatment and export to a pipeline. As gas storage entails explosion risks, gas is never stored on board a vessel but always compressed and routed onshore to power stations, etc.

”Technics' solutions are used to handle gas and Asia has many gas fields,” he added.

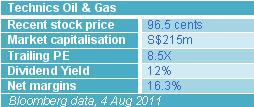

Yesterday, Technics announced a 3-cent interim dividend for 3Q11 (payable on 10 Oct), bringing the total dividend payable to-date for FY2011 to 12 cents per share.

Based on Thu’s close price of 96.5 cents, its dividend yield amounts to a very generous 12%.

The company’s financial year ends in Sep, and its 3Q11 revenue had increased by 66% year-on-year to S$45.7 million.

Gross profit margin in Q32011 was lower at 37% compared to 49% a year ago due to recognition of more contract engineering (CE) projects. These command lower margins compared to fast-tracked engineering, procurement, construction and commissioning (EPCC) projects.

Other than gas compression systems, Technics also handles EPCC projects for wellhead satellite platforms.

Operating expenses administrative expenses increased by 52% due to depreciation expense for a newly acquired plant and equipment and the administrative expenses of a new subsidiary.

Net profits were up 15%, at S$8.0 million.

Outstanding order book was S$103 million as at 3 August 2011, for progressive delivery through to 1H2012.

Below is a summary of questions raised at the meeting and the replies provided by managing director Robin Ting, executive director David Tay and group financial controller Maggie Lam.

Q: What is your market share for gas compressors in Asia?

About 80 to 100 gas compressors are produced in Asia each year and we can only produce 20 units a year. That makes our market share about 20% to 25%. Each FPSO needs two to four gas compression units.

Q: How long does one project last?

10 to 12 months

Q: What is the lifespan of your modules?

The lifespan of an FPSO is 30 to 40 years. Equipment lifespan however, is unpredictable, depending on the design and working environment. It also depends on how the operator uses it. Topside modules may be changed in 3 years or it could be as long as 5 years.

Q: The USD is heading down. How does this affect you?

We are naturally hedged. For USD contracts, we purchase raw materials in USD. Secondly, we use a lower exchange for costing. For example, when the USD is S$1.20, we cost it at S$1.15.

Q: If Europe collapses in the next six months, how will that affect you?

The USD will rise if the Euro depreciates. Our contracts are denominated in USD.

Q: If Europe collapses and America has a double-dip recession, how will that affect you?

Our business is in Asia. The funds will flow to Asia and this will beneift the valuation of our share price.

Q: There is a lot of positive news flow coming from Indonesia and Malaysia. Does that translate into more business for you?

Yes, we are getting more enquiries, especially from Sarawak. The projects there are firmed up and they are looking for tenders.

Q: Is Vietnam a key market for ASEAN ex Singapore?

Yes, they contribute about 50% to our segment revenue. We only have one customer there - VietSovPetro (VSP).

Q: Do you see a significant rise in VSP projects compared to last year?

Q: Do you see a significant rise in VSP projects compared to last year?

Yes. Vietnam is booming now.

Q: How does project delay affect you?

We are not really affected as customers pay at each milestone. Moreover, there is never project delay because customers are very concerned about continuous oil production.

Q: How does an increase in LNG price affect you?

If LNG prices rise, there will be more exploration demand for LNG and this will increase demand for our products and services.

Q: Can you elaborate on the aborted Treasury share sale to Serendipity?

The buyer could not fulfill the purchase conditions of depositing S$2 million by 22 Jul. We have never dealt with this party before.

Q: Can you explain how the dividend payout can be 140%?

This was projected based on annualized 9 months earnings. So far, we have not been paying final dividends.

Q: Can you explain the drop in cash balances (by S$14.0 million to S$11.8 million)?

We funded our subsidiary’s expansion.

Related story: Hot Stock: TECHNICS OIL & GAS Soars 9.6% On Heavy Institutional Buying

Anyway I don't expect 12% Div yield next FY but will be happy with 8-10% Div yield

I noticed that Technics leasehold property is carried at cost plus improvements at $7m. The Singapore yard at Loyang alone is worth more than $100m.

If land is revalued, the P/B become less than 1.5X, correct or not?