Excerpts from latest analyst reports...

AmFraser, in a rare call, initiates coverage of DYNA-MAC with a 'sell'

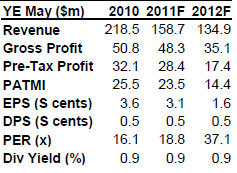

Analyst: Lee Yue Jer

Speculators’ Game: We initiate coverage on Dyna-Mac Holdings (DM) with a SELL and a fair value of $0.420.

We actually like the company for its strong technical capability, long track record and the large modern yard, but the current drought of new orders and the lack of earnings visibility beyond 1H2012 (i.e. Dec 2011) give us pause.

Further, the market is pricing Dyna-Mac at 15.7x historical P/E against a large-cap forward P/E of 13.6x, and the price today implies 100% yard utilization.

We believe the yard is operating under 50% capacity, which does not justify the valuations. We feel that there is a large element of speculation in today’s price, and we caution fundamentally-minded investors to steer clear. SELL.

Phillip Securities says Hu An Cable 'is unlikely to be another Chinese fraud'

Analyst: Chan Wai Chee

Two recently-listed peers are making evaluation of Hu An Cable that much easier.

The Shenzhen-listed companies have excellent disclosures, especially their half-yearly and annual reports. We find Hu An Cable performing smack-in with its peers in the last 15 months to 1Q11.

The strategy to move towards higher-voltage cables is ensuring survival of this peer group in a very competitive industry.Hu An Cable’s comparable performance means that it is unlikely to be another Chinese fraud, which usually outperforms peers by a big margin.

* High raw material prices and labour rates, together with a melee of competition at the low-end of market, reduced volumes of peer group. But moving to the high-end helps.

* Wire & cable industry leaders are confident their industry will outgrow China’s GDP growth for the next 10 years.

* Director Xu Guo Chen, who in his first year with the company, drew less than one-third of his last salary at his previous employ, must have seen greater potential here.

* We do not see as much concern as the others see in its copper rod business in terms of margin. If there are companies out there with huge margins, then the reader should better do more due diligence into those companies as margins are expectedly low.

We estimate Hu An Cable’s PV to be SG801m. Its current market cap is only SG250m.

However, as we understand the performance of this peer group, we only expect it to trade to 55% discount to PV (Present Value). This means an immediate target price of SG39¢.

Recent story: HU AN CABLE, XINREN ALUMINUM, ANWELL : Latest happenings

CIMB resumes coverage of MEWAH with 'outperform' rating

We see value emerging following Mewah’s recent decline. Mewah trades at 8.7x CY12 P/E vs. its peers’ 14.5x average.

Lacklustre 1Q11 results may have weighed on its stock, but we expect 2Q11 strength to serve as catalysts, apart from capacity expansion.

1Q11 volume accounted for just 21% of our FY11 estimate as unrest in the Middle East and Africa had disrupted trade, but inventories have run low and a wave of re-stocking should support a rebound in 2Q11.

We resume coverage with new earnings forecasts, an unchanged OUTPERFORM rating and a TP of S$1.29.

DBS says 'expect liquidity and funds flow into Asia to continue'

Analysts: Ling Lee Keng & Janice Chua.

Despite the steep run last week, our view for a more positive 2H11 remains. We expect liquidity and funds flow into Asia to continue to drive equities.

Our Singapore economist believes that 2Q is the worst quarter of 2011. 2H offers better growth momentum and tamer inflation compared to 1H.

Reconstruction in Japan, moderation in oil price, gradual recovery in US/Europe and sustained Asian domestic demand should paint a more positive backdrop for equities in 2H.

Comments