Montage photos: Haw Par

Could Haw Par stock be a ten dollar note available for sale at $6? Its book value as at end 2010 was roughly $9.80 while the stock recently sold for about $6.

Seasoned investors know the pitfall arising from investing simply based on discount to book value, no matter how huge the gap is.

Let's dissect Haw Par's two core businesses: 1) Operating businesses including property rental and sale of healthcare consumer products (mainly Tiger Balm's line of products); 2) Equity investments.

Market value of Haw Par = 197.9m shares x $6 = $1187.4m

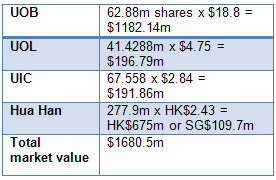

The company owns 4% of UOB (62.88m shares), 41.4288m shares of UOL, 67.558m shares of UIC and 277.9m shares of Hua Han biopharmaceutical which is listed on HKSE.

The market value of listed equities (as at 31 March 2011) is shown on the table on the right.

Total market value of listed equities = $1680.5m

Based on this, the business is discounted at a rate of 29%.

Not cheap enough? Here's some more icing - the company has no debt except income tax, both current and deferred. But for deferred tax, it probably isn't payable till its investment properties are sold but these are held for rental yield.

Haw Par holds $110m of cash. Add on this cash, and the business is selling at a discount of almost 34%.

In fact, the whole of Haw Par is just selling at slightly above the value of UOB shares that the company owns.

So, as in investor, at $6, you are simply paying for the UOB stake. You get the rest free - UOL, UIC, Hua Han, cash in the bank & investment properties + the Tiger Balm business which generates $79m in sales yearly.

Another method of valuation I use is based on earnings of both the operating business and the proportional share of earnings of its equity investments.

1) Operating business - Operating earnings excluding dividend from investments come up to about $36.5m. At a tax rate of 17%, net profit = $30.3m.

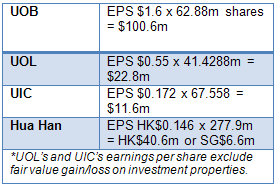

2) Proportion share of earnings from equity investments is shown on the table on the right.

Total earnings from operating business + earnings from equity investments on a look-through basis = $141.6m

On this basis, at $6 a pop, PE is less than 9.

Other considerations? Surely, there are. Are the equities that the company holds really valuable or undervalued for the matter? To be sure, it looks reasonable for the most parts, in particular, UOB - priced roughly 11x earnings.

What's the prospect of UOB? As long as Singapore and the region grows, UOB will grows too as assets in the region grows. Banks is simply just the money grid that helps to allocate and distribute capital from those who have them but don't need them to those that need them but don't have them.

Not long ago, Singapore government expressed the hope of increasing the nation's average salary by 30% on a real term in 10 years time or something.

This looks like one factor that looks favorable for banks to grow its asset base. Total assets was $214b at end 2010. ROA of 1.2% will produce $1.65 in eps. In 2001, UOB total assets was $114b. In 1992, was $28b. Part of it was due to merger like with OUB and most part to organic growth.

Need further proof? Here are some. Singapore GDP measured at current price was $84.7b and $304b in 1992 and 2010, respectively. A growth of 259%. UOB share price grew from $4.5 to $18.3 in the same period. A growth of 300%. Almost mirroring the country rate of growth

Update: Haw Par's stake in UOB may have increased from the previously reported 62.88 million shares during FY2010 by roughly 3.2%. Why? Because the actual "investment income received" as indicated in the cash flow from operation showed $6.282m during 2010, a huge reduction from $43.575m in the prior year.

The difference of $37.293m is almost equal to the portion of dividend that is due to her UOB's stake (62.88m shares X $0.60 dividend = $37.728). So instead of receiving the UOB's dividend in cash, Haw Par may have opted to receive it in scrip. Thus, Haw Par's stake in UOB may have ended as at 31 Dec 2010 with 62.88m shares x 1.032 = 64.89 million shares.

Moreover, it makes more sense to receive the dividend in scrip because

1) UOB is fairly inexpensive;

2) Haw Par will drown in cash if they are to keep receiving it without a good option to redeploy it;

3) it relieves the pressure of deploying cash for the sake of deploying it and end up with below-par investments;

4) the existing cash pile of $110m is more than enough to cover over 2 years of current dividend rate, excluding cash that will come in for the next 2 years from normal operations and other dividend other than UOB. Of course, the downside are for dividend seeking investors, there's less chance for an increase in dividend yield.

All in all, Haw Par seems to have made some sensible choices that position the company for better future value.

About the author Brian Chan:

Six years ago, I came across a biography of Warren Buffett which led me to the book, "The Intelligent Investor." That was the day I saw light and my proper education as an investor began. I've since became a dedicated die-hard-cast-in-stone intelligent investor. I'm currently a private investor who also help to manage money for my family members. I have no prior experience in the financial industry and am self-educated through reading Warren Buffett, Charlie Munger, Benjamin Graham, Walter Schloss, Howard Marks, and many other contrarian intelligent investors. I maintain a blog, http://berkshireh.blogspot.com, with occasional write-ups.