TWO QUITE different calls were made to the market yesterday (Apr 4): Based on fundamental analysis, Nomura Singapore said ‘buy’ stocks.

However, DBS Vickers had a ‘take profit now’ call based in part on technical analysis.

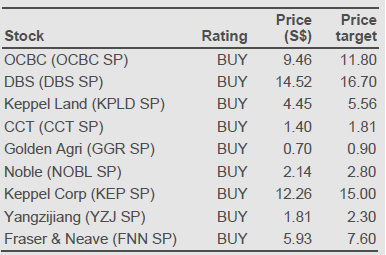

First, Nomura. The research team headed by Lim Jit Soon said the Singapore market has recovered 6% from its mid-March lows, but is still 3% down year-to-date.

“The market looks undervalued relative to history and poised to rerate, in our view, given persistent negative real interest rates. A strong S$ (+5% by year-end) and attractive market dividend yield (3%) should also boost returns for dollar-based investors.”

Its view was that investors should buy stocks of banks, commodities, offshore and office --- sectors that benefit from reflation and higher commodity prices..

See table at the top for its stock picks.

We note Nomura’s comment on Yangzijiang as being undervalued on an SOTP basis (non-core assets at book value on Nomura’s estimates).

“The market has under-appreciated the potential of a ~US$2.2bn containership order from Seaspan. While margins will likely be low, a successful execution of the potential order would be a significant technological breakthrough for YZJ.”

Nomura reiterated its BUY call and price target of S$2.30 on the shipbuilder.

As for DBS Vickers, here is what it said: “We maintain our view that a pullback for the STI in the immediate term is due. The 200-pt rally in two weeks is a little ‘too fast too furious’ and a pause to consolidate recent gains will be healthy.

“We also stick to our view that STI’s correction trend since November last year has ended at 2920 on 18 March. The anticipated pullback should find support at 3020-3045 first, before trending higher to the next resistance band at 3185-3210.

"While we believe that the stock market’s general direction remains up, albeit at a gradual pace, the usual concerns such as inflation, Europe’s sovereign debt or even a slowdown to China’s GDP growth will re-emerge to check the pace of ascend."

Whose views are you inclined to follow?

There was another cautionary voice yesterday - that of Asiasons WFG Research:

"After two consecutive weeks of increment, we may see some profit taking activity during the week, especially before the start of the results reporting season next week. As usual, attention will be focused on the US companies and would shift back to the Singapore companies as the US blue chips will release their results earlier than their Singapore counterparts.

"Judging from the economic releases over the past quarter, most companies are expected to continue their good performance in the past few quarters. This should improve market sentiment.

"However, as usual, we continue to remind investors to be cautious given that most of the negative factors affecting the stock market since the start of the year, i.e. China inflation, the Europe debt crisis and North Africa/Middle East's jasmine movement, were only repressed but not resolved. Despite being cautious, we still believe that the FSSTI has high chances to move towards 3,200 in April."

Recent story: YANGZIJIANG: A record US$2 billion contract to be inked in April/May?