BOCOM: GOLDEN EAGLE ‘top pick’

Bocom International said Golden Eagle Retail Group Ltd (HK: 3308) is its “top pick” in China’s consumer sector.

“We recently visited a few key department stores. Our channel checks found that: (1) store managers confirmed SSS (same store sales) growth slowdown in Oct 2011, mainly attributable to macro headwinds. This reinforces our less positive 2012 outlook; (2) Golden Eagle (GE)’s Nanjing Xinjiekou Store (XS) optimized its store layout with recent renovation to increase sales areas of gold and jewelry and cosmetics in Sept 2011.

“Golden Eagle remains our top pick in the sector. We were impressed by its good track record of store optimization efforts to revitalize sales growth of mature stores like XS.”

SSS growth slowdown

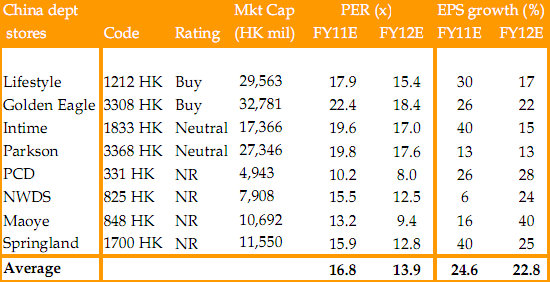

SSS growth of XS slowed from 14% in 3Q11 to 10% in Oct 2011.

For two key Springland (International Holdings Ltd; HK: 1700) stores, SSS growth rates also softened from 20% and 32-35% in 3Q11 to 16-17% and 27% in Oct 2011, respectively.

“Management attributed Oct 2011 slowdown to declining property prices, rather than the warm weather. Though our visit was on Friday, foot traffic in the stores, located at prime locations, was fair. We expect the increase of sales area of cosmetics and gold and jewelry sections to drive growth in FY12E.”

Golden Eagle’s Nanjing Xinjiekou Store. Photos: Bocom

Golden Eagle’s Nanjing Xinjiekou Store. Photos: Bocom

Bocom added that “good execution” from GE’s management supports the brokerage’s view of its premium valuation over peers.

“Though XS is a 16-year-old store with foot traffic already maturing two years ago, it still delivered decent high single-digit to mid-teen SSS growth from FY09 to 9M11 through ongoing store optimization efforts. GE management has had a good track record of optimizing mature stores like XS to revitalize sales growth.

“This reinforces our view that GE deserves to trade at a premium valuation over peers.”

See also:

TENFU: Tea For Two? Or Two Billion?

FOOD FOR THOUGHT: WANT WANT, TINGYI Noodle Blue-Chip Bound

MACQUARIE: PRC CONSUMER SECTOR To Trough in 1Q Macquarie Equities Research said it met with investors in the US to take the pulse of where they felt consumer sector stocks listed in Hong Kong were headed.

Macquarie Equities Research said it met with investors in the US to take the pulse of where they felt consumer sector stocks listed in Hong Kong were headed.

Investors generally expect slowdown on high base, macro concerns

Macquarie said that investors’ tone was “cautious,” though the brokerage thinks investors remain overweight on the consumer sector as they like the sector’s long-term growth story and better visibility.

“Most investors were very value driven and did not think valuation has been attractive enough to pull them into the sector, and thus intend to stay on the sidelines. For hedge funds, they welcomed short ideas.”

Macquarie added that in its view, a sector impetus, if any, would be driven initially by hedge funds.

Some disagree with expectation of possible luxury slowdown

Macquarie said it expects the luxury goods segment to see high growth volatility, and hence potentially more downside.

“However, the investors we met still see strong results from international brands. They are also interested in the Chow Tai Fook IPO, but do not agree with the high valuation, as the other small cap listed names trade at only half of Chow Tai Fook’s IPO valuation.”

Macquarie also said it had discussions about GOME given its low valuation and gross margin enhancement story, although investors were generally concerned about corporate governance issues.

For footwear, investors were interested in the competitive dynamic between Belle and Daphne.

Outlook

Photo: Chow Tai Fook

“We think the whole sector is likely to trough in 1Q12 with the end of the downward earnings revision cycle. The valuations should then become more attractive and investors could more aggressively add to their positions,” Macquarie said.

It added that it likes the market leader in each segment, contending that they have the potential to be the consolidator when the market is in a cyclical downcycle.

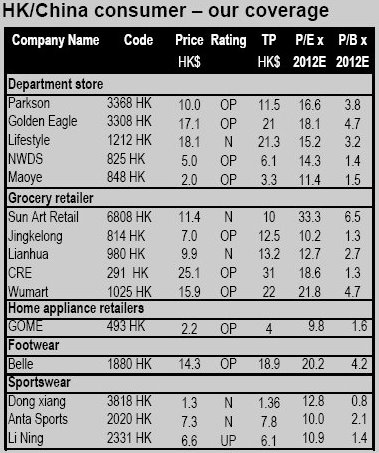

Macquarie’s “top picks” remain Golden Eagle (3368 HK, OP, TP: HK$21.0), Belle (1880 HK, OP, TP: HK$18.9) and GOME (493 HK, OP, TP: HK$4.0).

See also:

Regime Change: CHOW TAI FOOK Founder To Become Richest Chinese

BAOFENG: Aiming To Crystallize New Orders With Swarovski