Excerpts from latest analyst reports.....

Phillips Research says 'buy' C&O Pharmaceutical as a takeover target

Analyst: Toh Wei Kiong

• Strategic investment by Sumitomo Corporation

• Prelude to a full take-over?

• Deal beneficial to C&O business

• Maintain Buy and fair value of S$0.65

C&O announced on 1st December 2010 that Sumitomo Corporation has bought a 29% stake in the company from the controlling shareholder, Mr Gao, at a price of S$96.2m or S$0.50 per share. On the business side, C&O will be able to benefit strongly from the expertise of Sumitomo Corporation; 1) as a supplier of drug ingredients to domestic and overseas drug makers and 2) broker of technologies and products in the R&D segment. More information of Sumitomo Corporation can be found on their website, www.sumitomocorp.co.jp.

How will this deal benefit C&O

1. Sumitomo Corp will act as broker to bring in new drugs that are currently circulated in Japan, US and Europe to be distributed by C&O in China; 2. Sumitomo will introduce Japanese drug makers who are seeking entry into China to C&O who will then help these companies conduct clinical trials and testing;

3. Once approval is given for the drug, C&O will then obtain licensing rights from these companies to distribute the drugs in China;

4. Provide Active Pharmaceutical Ingredients (API) to C&O for production of generic drugs.

Under the Singapore take-over code, a company is required to make a general offer for the company once its shareholding exceeds 30% in the target company which puts Sumitomo Corporation 1% away from making a general take over offer for C&O. Furthermore, Mr Gao (majority owner) will be relinquishing his role as the Chairman of the board to the new executive nominated by Sumitomo and take on the role of Vice-Chairman.

We think that this strategic investment is a prelude to a full take-over once Sumitomo Corporation is confident with C&O’s operations and distribution strength. We are advising shareholders to hold or accumulate the stock as valuation right now is still very attractive and the potential of new drugs being injected at a faster pace will contribute positively to the earnings for C&O.

Valuation and Recommendation

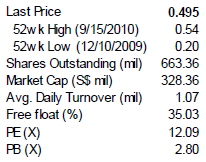

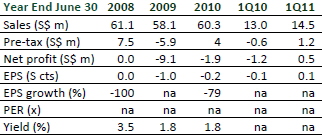

We are maintaining our Buy recommendation and our fair value estimate of S$0.65 using the discounted cash flow model (unchanged). There is no change to our earning estimates for now until we receive more information regarding the type of drugs to be introduced into the Chinese market. C&O is currently trading at a P/E of 11.8X FY10 earnings and 10.6X FY11 expected earnings, which is a steep discount to its peers who are trading at an average of 42X trailing 4 quarters EPS. Our fair value of S$0.65 translates to a P/E of 13.7X FY11E expected earnings.

CIMB says buy CHINA ANIMAL HEALTHCARE (37 c) with target price of S$0.52

Analyst: Gary Ng

• Maintained BUY. CAL exhibits significant potential in the PRC veterinary industry. There are four mandatory vaccines that the PRC Ministry of Agriculture has approved for administration to livestock. Apart from being the biggest powdered animal drugs producer in the PRC, CAL also owns three of the mandatory licenses, further strengthening its market position.

Our target price remains at S$0.52, derived from a target multiple of 10x CY11 P/E, keeping the stock at a 50% discount to industry average due to its relatively smaller size than its PRC peers.

• We believe that CAL’s investment merits lie in its (i) strong industry traction; and (ii) a sound market expansion strategy, (iii) and CAL does offer excellent value trading at.6.6x CY11 P/E against its 3-year core earnings CAGR forecast of 41.1%.

We see stock catalysts from (1) fast track expansion through M&A of key vaccines producers, (2) higher trading multiples from the dual-listing in HKSE, and (3) increased interest from institution investors.

Recent story:CHINA ANIMAL HEALTHCARE, AEI CORP: What Kevin says.....

Kim Eng Research says LC Development has a near-term catalyst

Analyst: OOI Yi Tung

Xuzhou is the next catalyst. The company, together with a Chinese JV partner, is embarking on a mixed development project in Xuzhou that consists of 12 blocks of luxury apartments, a megamall, a Grade A office tower and a five‐star hotel. The residential component will take up at least half of the total GFA of 277,000 sq m and will be launched for sale in phases beginning in mid‐2011.