CHINA'S TEXTILE industry is clearly rebounding, as the Q1 results of four Singapore-listed companies, which were released yesterday evening, clearly show. On 6 April, we had an article that pointed to the trend: CHINA TEXTILE: No longer hanging by a thread, watch out for 1Q results.

The Q1 results of 2 companies - China Taisan, China Gaoxian Fibre and Li Heng Chemical Fibre - are captured in the tables below. More importantly, the companies are giving guidance of a bullish 2010.

(The full results of these companies as well as another company, Hongwei Technologies, can be viewed at the Singapore Exchange website www.sgx.com)

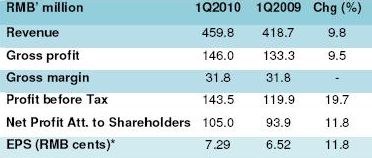

CHINA TAISAN's sales grew 51.0% year-on-year to Rmb 302.5 million due to rising average selling prices and a higher sales volume. higher than 1Q10, and the financial performance for FY2010 will be better than FY2009.

Weighted average selling prices rose 6.6% year-on-year due to higher average pricing for both performance fabrics and fabric processing services.

Sales volume jumped 41.5%, driven mainly by the successful launches of new products in 2009.

The new products contributed over 20% of the group sales for 1Q2010, and provided better gross profit margins. China Taisan launches three to five new products every year.

Orders are pouring in from manufacturers for fast-growing domestic sportswear and casual wear brands in China, such as Metersbonwe, Anta, Xtep, and 361-degrees, according to China Taisan.

The leading Chinese maker of knitted fabrics for sporting apparel has an outstanding order book of about Rmb 247.0 million, which is scheduled for delivery over the next two to three months.

With this order book, the management expects utilization of its production lines to stay above 85% for 2Q2010.

Barring any unforeseen circumstances, the Group is optimistic that the revenue for 2Q10 to be

“2010 would be a very busy and robust year for China Taisan”, said CEO Lin Wen Chang.

The company's Q1 net profit is about S$22 million, which translates into about $88 million on an annualised basis. Yet the market has accorded the stock a PE of only abut 2.5X.

China Goaxian chairman and CEO, Cao Xiangbin, can only hope that as his business delivers strong results, the market would re-rate his stock. And the outlook does seem promising.

“As a leading supplier of premium differentiated polyester yarns and fabric products, we look forward to benefit from the rebound in domestic demand relying on our strong foothold in domestic markets and fast expansion.

"In order to meet growing domestic demand, we are on track to execute our production capacity expansion plans as stated in the IPO prospectus, all the balance IPO proceeds is planned to put into use this year,” he said.

The Group has purchased a total of 100 WKF machines. The purchase was made using RMB171.5 million (equivalent to approximately S$34.5 million) out of the S$78.3 million raised from the IPO proceeds.

The Group expects 50 of such new machines to start operation in 3Q2010, with the balance 50 WKF machines in 4Q2010.

Such a rapid expansion will boost the Group’s maximum annual production capacity for WKF 4.8 times from 17,000 metric tonnes to 81,000 metric tonnes after full installation of the machines by end 2010.

In addition, the Group plans to acquire 72 new machines in 2H2010 for the production of its premium differentiated yarn products to expand maximum annual production capacity to approximately 240,000 tonnes.

Recent story: HONGXING, TAISAN, GAOXIAN to benefit from China's sports push

LI HENG CHEMICAL FIBRE says the textile and garment industry in China has continued to recover and the Group noticed a gradual improvement in both demand and Average Selling Prices of its nylon yarn products.

However, the Group is cautious on the timing and scale of a full recovery and the impact of China's anti-dumping tariffs on imported PA chips (raw materials for Li Heng's business) remain uncertain.

Gross margins of Li Heng’s nylon yarn products remain depressed as compared to earlier years and raw material costs are increasing at a faster rate than the increase in ASPs of nylon products.

Notwithstanding the uncertainties, the Group believes the expansion in Liheng Phase III will enlarge its revenue and profit base and partially mitigate the negative effect of the risks of increasing raw material cost and lay a strong foundation for long term, sustainable growth.