THIS WEEK, we feature Chip Eng Seng (CES), which evolved from its contractor background into an integrated developer in the last decade.

Chip Eng Seng (82.5 c) trades at 5.95X trailing PE and a 4.94% dividend yield. Chart: www.ft.comCES rode the last property cycle and raked in a combined net profit of some SGD300m during 2010-11, boosting shareholders’ equity by 2.5 times over that two years.

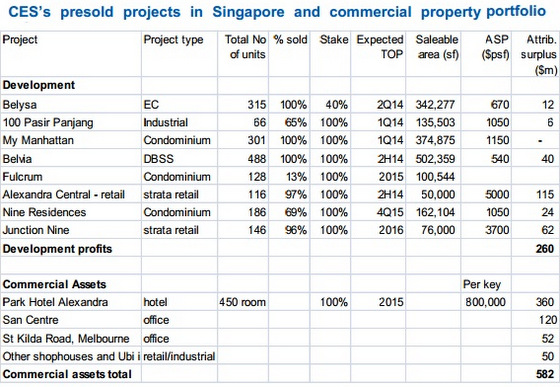

Chip Eng Seng (82.5 c) trades at 5.95X trailing PE and a 4.94% dividend yield. Chart: www.ft.comCES rode the last property cycle and raked in a combined net profit of some SGD300m during 2010-11, boosting shareholders’ equity by 2.5 times over that two years.The group obtained T.O.P for its industrial project 100 Pasir Panjang and condominium project My Manhattan in the first quarter of this year, and is on track to complete Belysa (EC project), Belvia (DBSS project) and Alexandra Central retail in the course of 2014.

In 2015-16, the group will complete its mixed development project at Yishun (Junction Nine/Nine Residences), its Alexandra Road hotel and Fulcrum, a mid-market residential project. With the exception of Fulcrum, CES’ other projects are substantially sold with healthy margins.

Chip Eng Seng Corp CEO Raymond Chia.

Chip Eng Seng Corp CEO Raymond Chia. Photo: InternetFor its hotel at Alexandra Central, the group has appointed Park Hotel Group as the hotel manager. Against a development cost of SGD208m, cost per room works out to SGD460,000 for the 450-room hotel.

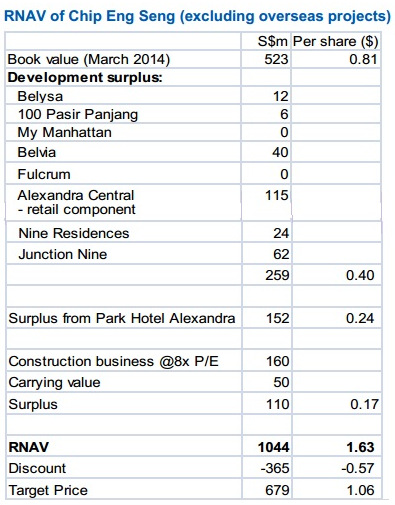

Given the recent transactions of 3-4 star hotels in the city fringe, we believe CES’s hotel is easily worth at least SGD360m based on SGD800,000 per key. This implies a potential revaluation surplus of SGD152m.

The bulk of the profit contribution comes from two mixed development projects. The first one is the strata-titled retail units at Alexandra Central, which sold between $4000-8000 psf at the height of the craze for commercial properties in early 2013. Net profit from the development alone will contribute SGD114m, by our estimates.

The second project, Junction Nine and Nine Residences in Yishun, should gross over SGD86m when completed in 2015/16.

|

|

http://www.nracapital.com/research/sgxresearchreport/1408mne6jh

By Q3 2014, CES' s actual 9mth NAV was already 91 cents but NRA full year NAV forecast was only 92.6 cents.

I expect CES full FY14 EPS to hit 38 cents, and full-year NAV to hit ~$1.10, but NRA full year EPS forecast was only 27.5 cents, NAV was only 92.6 cents

Even the Phillip Capital Report is deemed to be conservative as it had not taken into account the following into its RNAV computation

http://www.uniphillip.com/development/modulespdf/webinars/PSR%202014-08-25%20(Lantro,%20OCBC,%20Value,%20PanUtd,%20Boustead,%20Chip%20Eng%20Seng).pdf

1. THREE land banks in Australia

2. Profits from TM (even if the project is called, rental yield is ~8%)

3. Profits from Fernvale projects

4. Revaluation Gain from CES centre

5. Recurring income is grossly understated...

6. CES also has its HQ at Ubi and some shop houses at Geylang

7. Profits from Fulcrum

8. Monetization of hotel in the near future..

The RNAV of CES is easily more than ~$2

Can we conclude that Mr Market has already priced in this event?