This article was posted recently on remisier Ernest Lim's blog, http://www.ernestlim15.blogspot.com/, and is reproduced with permission.

Leader Environmental (“Leader”) shares plummeted 45% from an intraday high of $0.230 on 1 Jul to an intraday low of $0.127 on 19 Jul. It subsequently rallied 57% to an intraday high of $0.20 on 27 Jul.

Before this roller coaster ride, I believe most retail investors have not heard of Leader. Firstly, the company is an S-chip with a market capitalization of only SGD94m.

It does not have an investor relations firm and does not publish any company contacts for shareholders and potential shareholders.

Currently, Leader is covered by one analyst from DMG.

What piques my interest in this company is the industry that it is in.

Companies such as Leader which provides environmental protection solutions seem to be in a sweet spot, especially as China aims to establish an environmental friendly society in their 12th Five-Year Plan.

I managed to arrange an appointment with Mr Lim Poh Yeow, Leader’s CFO (“Management”) for a 1-1 discussion on Leader’s business and prospects.

Below are the key takeaways from the meeting.

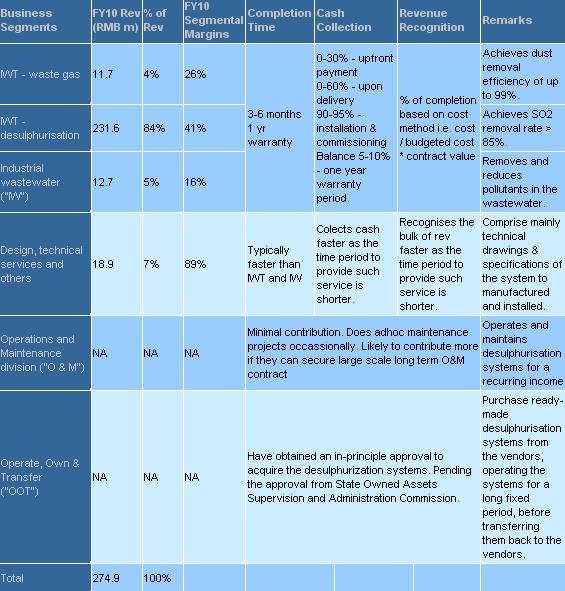

Firstly, Leader is principally engaged in the research and development, design, manufacturing, assembly, installation, and support services of environmental protection systems, primarily for industrial wastegas and wastewater emissions.

Quite a handful, isn’t it?

I have summarised the business segments and the targeted segments which Leader wants to enter in the near future in Table 1. O&M and OOT business are the targeted segments which Leader is entering in the near future.

Price slumped due to…

Management is puzzled about the plunge in its share price. However, he assured me that the company’s fundamentals remain sound.

As they are in a growing industry, there is no lack of contracts but the company is choosing contracts with better margins. In response to this, I pointed out that Leader has not announced any new contracts since 10 May.

Management explained that Leader typically announced contracts when they have a cumulative size of around RMB100m.

As the contract award season is usually around April to August, it is likely to have more updates on its order book and new contract wins in the next 1-2 months.

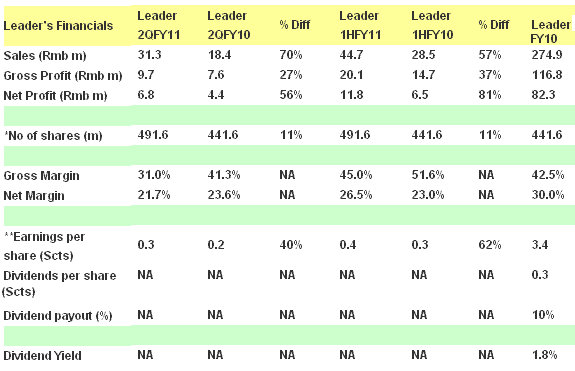

Furthermore, the drop in share price is also unlikely to be due to its results as Leader announced a good set of 2QFY11 results. 1HFY11 revenue and net profit after tax jumped 57% and 81% respectively to RMB45m and RMB11.8m respectively.

Table 2 shows the summarized results.

Based on Table 2 above, Leader 1HFY11 significantly lags behind its FY10 results.

However, it is noteworthy that Leader’s 2H results are typically stronger than 1H.

This is because Leader’s mainly operates in the northern parts of China where they usually experience harsh winter conditions from Dec to Mar.

As a result, Leader undertakes most of their manufacturing and installation works between April and November. Thus, 2H is usually much stronger than 1H.

Partly due to the lumpiness of their existing business, Leader is venturing into the O & M and OOT business so as to generate a more stable stream of revenue and income.

According to a DMG report, the OOT business may generate gross margins as high as 40%. Nevertheless, the O & M and OOT are still a “work-in progress” stage and we would have to wait for further updates on this.

May be worth a look for investors keen in China’s environmental industry

For investors who are interested in China’s environmental industry, yet are not afraid of taking S chip risk, it may be worth their while to take a deeper look into this company. According to Bloomberg, Leader trades at FY11F PE of 3.6x.