Excerpts from latest analyst reports....

NRA Capital says accumulate Cheung Woh Technologies

Analyst: Lee Khai Chian

Cheung Woh (“CWM”) has divested its 36.4% stake in Tysan Precision (“TP”), an automotive component manufacturer in the PRC. We view the divestment to be value-accretive to shareholders. At current price level, it is attractive enough to accumulate on three reasons.

HDD business still growing. CWM is set to benefit from potential increase in demand that ensues from the acquisition of Hitachi Global Storage Technolgies by Western Digital (“WD”), which is expected to complete in 1Q2012. CWM is currently increasing its headcounts in Johor plant by almost 50%, in anticipation for the surge in order from WD in 2012.

Improve cash flow and lighten asset. Free cash flow will improve following the divestment. As TP will be accounted for using equity method, capital tied up to daily operation will be trimmed tremendously as collection days for automotive business range from 180 to 200 days, much longer than 60-80 days for HDD.

Furthermore, CWM will become more asset-light once the capital intensive automotive business is deconsolidated from the group balance sheet.

Of note, PPE and borrowings will be reduced by 30% and 50% respectively after the exercise. Meanwhile, capex will drop considerably to $4m in FY12, as compared with $19m in FY11, S$15m each for both FY10 and FY09.

Share buyback and special dividend. TP will become a 33% associate company after the divestment. CMW will receive US$9m proceeds, which will likely be used for share buybacks and special dividend.

As the share price is currently trading below NTA per share of 30 cents, we believe the exercise is worthwhile.

Additionally, special dividend is indisputably on the table, given the reduced capex in the years ahead and less working capital requirements. Therefore, dividend per share for FY12 in our view, will conservatively be at least on par with last year’s 1.5 cts, offering at least a 6.3% yield.

Valuation. The results for second quarter this financial year is likely comparable to the preceding quarter as the easing of supply chain problems nullify a seasonally weaker quarter. The counter is currently trading at 4x consensus FY12 PER and 3.5x FY13 PER.

Recent story: CHEUNG WOH: Realizes investment in auto unit to focus on HDD

DBS Vickers upgrades OKP to 'buy' and 80-cent target

Analyst: Suvro Sarkar

Photo: OKP

Given the healthy 15% EPS CAGR over FY10-12, we upgrade the stock to BUY with TP revised up to S$0.80, based on 1) 7x FY11/12 blended PE for its recurring business and ii) estimated S$0.23 per share surplus cash.

OKP currently has about S$97m net cash on its books (S$0.32 per share), and dividend yield looks attractive at about 7.7%.

Interim dividend of 1Sct (in line with FY10) has already been declared.

Re-rating catalysts could come from deployment of surplus cash towards M&A activities to drive vertical integration, or even towards investments in property developments.

Recent story: ANWELL stock up 100% in 5 weeks, OKP's half-year profit up 56%

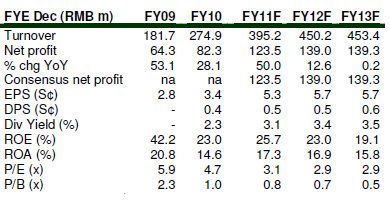

DMG says panic selling of Leader Environmental Technologies (LET) unwarranted

LET posted a strong set of 2Q11 results with RMB31.3m in revenue (+69.8% YoY) and RMB6.8m in net earnings (+55.9% YoY).

Desulphurisation Engineering, Procurement and Construction (EPC) business continues to power growth, making up 85.5% of the group’s 1H11 sales.

The bulk of its earnings (>80%) come in the second half. EPC order book currently stands at RMB100m, and we expect the group to secure another RMB250m worth of EPC contracts by the end of August.

Reiterate BUY, with a TP of S$0.47 (previously S$0.53), based on 8.9x P/E (-1 SD industry P/E).

Unwarranted market panic, auditors give clean bill of health. The share price has dived more than 30% since May. It is clear to us now that the recent panic sell-down was unwarranted, making LET a bargain.

There are two main reasons behind our belief on top of the group’s solid fundamentals.

First, none of the major pre-IPO investors have reduced their shareholding even though the blockout period is over, casting their vote of confidence in LET. Second, both their external and internal auditors, Ernest & Young and Grant Thornton respectively, have audited LET’s account recently and have given it a clean bill of health.