Excerpts from latest analysts reports....

OCBC says VIKING’S fair value is 32 cents

Analyst: Low Pei Han

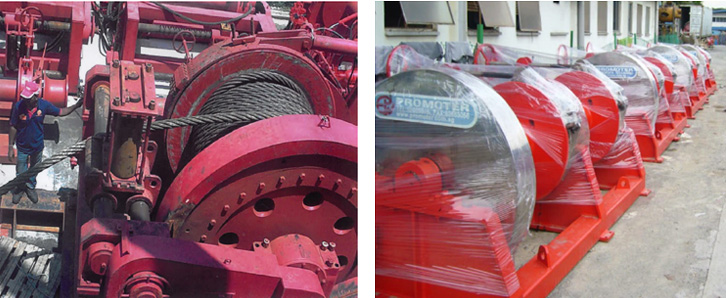

Viking Offshore & Marine (Viking) reported a 112% rise in revenue to S$79.7m and saw a 14-fold increase in net profit to S$12.6m in FY10.

Net profit was 0.2% shy of our full year estimate, and exceeded management’s guidance of S$10.5-12m.

We estimate core net profit was about S$4.9m vs. approximately S$1.1m loss in FY09.

With the recovery in rig orders, we understand that Viking has already secured work from recent rig contracts won by Keppel Corporation. The group also signed S$24.8m worth of contracts with overseas customers in 2010.

The swift pick-up in new rig orders has meant that a challenge for the group and its competitors may be an impending labour shortage rather than a lack of jobs.

Going forward, we will focus on Viking’s integration process, its ability to execute projects well and control costs. A first and final dividend of 0.3 S cents has been proposed, representing about 13% of FY10’s net profit.

Maintain BUY with SOTP-based fair value estimate of S$0.32.

Recent story: VIKING OFFSHORE & MARINE: Why it's 20% of my portfolio

CIMB ups BROADWAY’S target price to $1.84

Analyst: Jonathan Ng

Nevertheless, we raise our FY11-12 estimates by 1% after incorporating higher sales but lower margin and effective tax assumptions. We also introduce FY13 forecasts.

Following our upgrade, we have a slightly higher target price of S$1.84 (from S$1.82), still valuing Broadway at 8x CY12 P/E (within its 5-year trading band). We expect a 2H11 earnings recovery to provide stock catalysts.

Recent story: BROADWAY, INNOTEK: What analysts say now.....

DMG expects TDR listing to trigger stock price increase for SINO GRANDNESS

Analyst: Tan Han Meng, CFA, CPA

Sino Grandness (SFGI) announced yesterday that it is planning to offer and list Taiwan Depository Receipts (TDRs) on the Taiwan Stock Exchange representing a number of ordinary shares of the company to be decided by its Board.

Our study on eight SGX-listed companies that are recently dual-listed in Taiwan suggests it takes an average 150 days from first announcement of TDR plan to eventual dual-listing, with share price in Singapore appreciating an average of 16% during the period.

In particular, consumer-related counters Oceanus (BUY) and Super (NEUTRAL) saw positive returns of 21% and 40% respectively.

We think SFGI’s dual-listing could possibly take place coming Jun-Jul (assuming necessary approvals are obtained) and believe its share price will react positively to the event in the near-term.

Maintain BUY at TP of S$0.68, pegged to 6x FY11F P/E. SFGI is due to report its 4Q10 results on 22 or 23 Feb.

Recent story: BRIGHT WORLD, SINO GRANDNESS, UMS: What analysts now say.....