Excerpts from KGI report

GEO ENERGY (GERL SP): Winter is coming

BUY Entry – 0.27 Target – 0.42 Stop Loss – 0.24

|

Geo Energy |

|

|

Share price: |

Target: |

Geo Energy is one of Indonesia’s leading coal producers. The company has four mining concessions located in South and East Kalimantan. Geo Energy’s two key mines have a total estimated coal reserve of 84 million tonnes, based on a Joint Reserves Committee (JORC) Compliant report issued in December 2020.

-

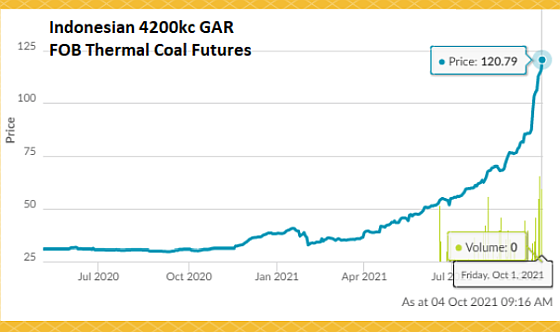

Coal prices are going ballistic. Geo Energy is set to have a record year ahead as coal prices have essentially gone through the roof. ICI 4 prices (4,200 kcal) are at more than 10-year highs, gaining almost 80% YTD. Current dynamics are very favourable for coal miners given the shortages being experienced in India and China.

On the supply side of the question, there’s less risk of an oversupply-related correction for coal markets as ESG pressure has pushed capital towards clean energy (e.g., solar, electric vehicles, wind farms), thus limiting rapid coal supply growth. Chart: www.sgx.com/derivatives/products/thermal-coal

Chart: www.sgx.com/derivatives/products/thermal-coal- Cash generating machine. We estimate Geo Energy will generate at least US$247mn (S$333mn) of free cash flows in 2021 and 2022, almost equivalent to its current market cap of S$385mn. Our estimates are based on US$58/US$50 coal prices and 10.5mn/11.0mn tonnes of coal production in 2021 and 2022, respectively.

Our assumptions are very conservative given that current ICI4 future prices are trading well above US$100/tonne. Even when accounting for the domestic market obligation (25% of production volume) where prices can be as much as 60-70% discount to export prices, our assumption of US$60 and US$50 per tonne for 2021 and 2022 is very conservative.

We currently have an Outperform and DCF-backed TP of S$0.42 on Geo Energy. Our fair value is based on DFC with a conservative set of assumptions:

1) 13.5% discount rate,

2) six-year mine life up to 2026, and

3) no terminal value.

The strong cash flows over the next two years will provide the group options to diversify via acquisitions. The group currently trades at an average 3x P/E for 2021-2023F and offers an above-industry dividend yield of 8%, 5% and 4% for 2021-2023F, based on a conservative 30% payout ratio.- Read our full report here.

- Cash generating machine. We estimate Geo Energy will generate at least US$247mn (S$333mn) of free cash flows in 2021 and 2022, almost equivalent to its current market cap of S$385mn. Our estimates are based on US$58/US$50 coal prices and 10.5mn/11.0mn tonnes of coal production in 2021 and 2022, respectively.