|

Koda – Clear beneficiary of surge in home furnishing trend |

Chart: Yahoo!It is noteworthy that Koda is an Original Design Manufacturer / Original Equipment Manufacturer for its customers in North America.

Chart: Yahoo!It is noteworthy that Koda is an Original Design Manufacturer / Original Equipment Manufacturer for its customers in North America.

In fact, customers in the North America region constitute approximately 55% of its FY20 revenue.

Its forte is in home furniture, and it is possibly the largest dining room furniture exporter in Southeast Asia. Home furnishing seems to be in demand as consumers stay at home and have more disposable income to spend (rather than travel) to improve their homes.

Koda’s 1HFY21 revenue and net profit jump 16% to US$39.6m and US$4.8m respectively on good demand for furniture.

Given this promising backdrop, it may be timely to take a closer look into Koda. I had the privilege of meeting Mr Joshua Koh, CEO of Commune Lifestyle Pte Ltd and Mr Kenny Zhang, CFO of Koda (“Management”) for a 1-1 discussion over Koda / Commune’s operations and prospects via Zoom.

Below is my personal interpretation of my discussion with Koda’s management and my own inferences from Koda’s announcements on SGX.

Koda's & Commune’s background

Koda was established in 1972 by Mr Koh Teng Kwee. It started by producing wooden TV and speaker cabinets. Koda has progressed from being an Original Equipment Manufacturer (OEM) to an Original Design Manufacturer (ODM). Its forte is in home furniture, and it is possibly the largest dining room furniture exporter in Southeast Asia. Besides its ODM business, Koda established Commune Lifestyle Pte Ltd in 2011. This is their in-house brand and managed by the 3rd generation of the founding Koh family. Commune has a presence in Singapore, Malaysia, China, Philippines, and Hong Kong. Readers can refer to the respective websites for more information on Koda (click HERE) and Commune (click HERE). Koda has been listed on SGX since 18 Jan 2002. |

What is so interesting about Koda?

Outlook continues to be bright

Based on 1HFY21 results (financial year ends in June), management continues to see encouraging growth in their export orders and they expect the capacity utilisation rates for its key factories to remain consistently optimal. This is attributed to generally higher demand for furniture arising from work-from-home arrangements.

Their recent proposed acquisition of Land Use Right and a factory building in Long An Province, Vietnam (announcement dated 25 Mar 2021) to expand their production capacity corroborates the positive momentum that they are seeing in their business.

Margins are likely to be steady amid strong demand

Notwithstanding the rise in costs of timber, fabric, metal frame, foam, and shipping etc, Koda believes that they should be able to maintain their current gross profit margins (“GPM”) of around 30 - 32%.

This is because, firstly, it can pass on such costs to the customers amid strong demand. Secondly, their Commune business has GPM of around 50%. As this segment grows and becomes more significant, it may even be able to raise its overall GPM to above 30 - 32%.

Multiple growth drivers

Besides its export orders, Koda has a couple of other growth drivers. Firstly, Commune is currently their largest growth driver which Koda continues to expand steadily (please refer to my next point on steady expansion in China).

Secondly, Koda has launched its Alto brand in late 2019 to serve customers who wish to have larger, more exquisite, and luxurious furniture in their homes.

Thirdly, the Group had in 2019 purchased land use rights (as announced on 14 November 2019) which a sofa factory will be built to cater for sofa business. Currently, the sofa manufacturing is carried at a rented factory. Once the sofa business gains traction, a sofa factory will be built.

Progressive and steady expansion in China

In Aug 2017, Koda announced that it plans to increase its China presence from 43 Commune stores to up to 100 by 2020. Due to Covid 19 and partly because of Koda’s prudent management, Koda has not met its target of 100 Commune stores yet.

Nevertheless, the expansion has been steadily on-going. As of now, Koda has approximately 75 Commune and Alto stores in China. Readers can refer to how Koda / Commune expands into China via this informative article (click HERE). It is noteworthy that Commune and Alto stores fetch higher GPM than its ODM / OEM segment.

Trades at attractive valuations based on both PE and P/BV

Based on my “back of the envelope” estimates, notwithstanding the temporary shut-down of their Malaysiam plant in Feb and now in May / June (based on the assumption that Covid does not worsen) + seasonal effects of Chinese New Year, I guess 2HFY21F should be probably on par or just slightly weaker than 1HFY21. Based on its annualised FY21F earnings, at $0.700, Koda trades at approximately 4.6x FY21F PE and 0.95x P/BV. Based on Shareinvestor, Koda’s net asset value per share is around $0.735.

In comparison, Man Wah (01099.HK), which is in a similar industry, trades at 30.4x FY22F PE and 5.9x FY22F P/BV.

Man Wah is significantly larger, and it is not a direct comparable. However, the stark difference in their valuations is glaring and interesting.

Net cash – comprises approximately 1/3 of its market cap

Based on 1HFY21 results, Koda has net cash of US$14.3m which represents approximately 1/3 of its market cap (market cap is around S$58m). Based on my personal estimates (note I’m not an analyst hence do take my estimates with a large pinch of salt), Koda trades at 3.1x ex-net-cash FY21F PE on an annualised FY21F earnings.

By any standards, this seems to be extremely low given the bright outlook. I.e. FY21F strong earnings may not be one off.

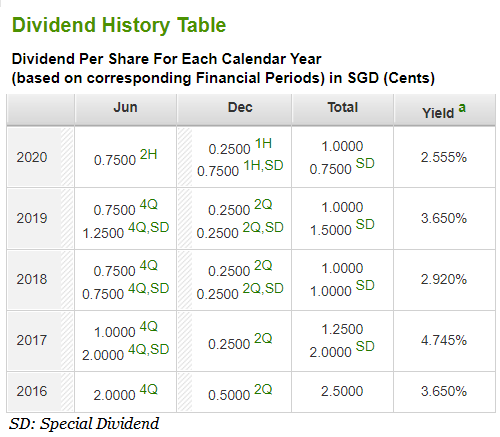

2H dividend is typically at least 3x that of 1H dividend

Based on Fig 1 below, it is apparent that Koda’s 4Q dividend is typically at least 3x that of 2Q dividends. The exception is 4QFY20 (CY June 2020) but that is during Covid 19. If I annualise Koda’s 1HFY21 results, FY21F revenue and net profit are likely to be around US$79.1m and US$9.6m respectively.

From FY16 to FY20, the highest revenue and net profit generated are US$60.4m and US$5.4m respectively.

Hence FY21F is likely to be the highest for the past few years. Thus, if historical pattern proves to be accurate, 2H dividend may be probably three times that of 1H dividend.

If Koda dishes out $0.03 / share in 4QFY21F, then its full year dividend yield works out to be 5.7%!

Nevertheless, I wish to add a caveat that this is a very rough and simplistic gauge only. Readers who are financially savvy can calculate the various dividend pay-out ratios for the past years and ascribe an average dividend pay-out to FY21F earnings so as to estimate 4QFY21F dividend.

Fig 1: Koda’s dividend history for the past five years

Source: Shareinvestor 1 Jun 21

Risks

As with (almost) all investments, they carry risks. Below are just examples of some noteworthy risks.

Illiquid with daily average 30D volume amounting to 20K shares

Notwithstanding the two bonus shares issuance in 2017, Koda’s shares are thinly traded. Average daily 30D volume amounts to 20K only. This is not a liquid company where investors with meaningful positions can enter or exit quickly.

No rated analyst coverage

During 2007 – 2008, Koda was covered by a few brokerage houses, namely OCBC, Maybank and RHB. However, Koda’s results weakened after the global financial crisis in 2009-2009 and analysts gradually dropped coverage. As of now, there is no rated analyst coverage on Koda even though this year is likely to be a year with multi-year high results. Notwithstanding Koda’s long operating history, it is likely that some investors and fund managers are still not familiar with Koda’s business and prospects, thus it may take some time for Mr. Market to get to know this company.

Production may face bottleneck if Covid worsens

Malaysia Government has imposed a 14-day Movement Control Order (“MCO”) from 25 May 2021 to 7 June 2021. However, on 28 May, Malaysia tightens the MCO to become a full nationwide lock down from 1 – 14 June 2021. Based on Koda’s announcement dated 31 May 2021, Koda will be closing its factories located in Senai, Johor temporarily. Although the Group acknowledges that the closure will result in lower production output for the Malaysia Operations in the month of June 2021, it is not expected to have a significant impact on the Group’s financial performance for the financial year ending 30 June 2021, barring unforeseen circumstances. Nevertheless, should Malaysia continue its nationwide lockdown to more than a few weeks, its production may be affected to a larger extent, and it may have an adverse impact on Koda.

Possibility of shipment delays if the shortage of containers worsens

Based on 1HFY21 results, management observes that there are increasingly higher shipping costs and shipment delays across several industries due to the shortage of containers. If the shortage of containers worsens, or persists for an extended period of time, this may affect Koda to some extent.

Small market cap of S$58m

Koda is a company with an approximate market capitalisation of S$58m. With its small market capitalisation and illiquid nature, it may be difficult to attract analysts and fund managers’ attention.

Order visibility

Unlike those companies in the shipbuilding, construction, or technology industries where they have order books stretching more than one year, Koda usually only has a few months of visibility as they deliver fast to customers and customers do not usually order 1 – 2 years in advance or wait for furniture for 1-2 years. However, amid the strong demand that they are seeing now, Koda has at least six to nine months of order visibility.

Conclusion Ernest Lim CFA, CA (Singapore)Koda seems to be in an industry which is seeing strong demand. Ernest Lim CFA, CA (Singapore)Koda seems to be in an industry which is seeing strong demand. Trading at attractive valuations, net cash and with a likely good dividend yield, this company looks interesting. However, its illiquidity and possibility of production bottleneck (due to Malaysia’s lock down) are some of the risks that readers need to be aware of. |

Disclaimer

Please refer to the disclaimer HERE

This article was originally published on Ernest Lim's blog.