|

BHG Retail REIT ("BHG" or the "REIT") is offering 151.169m units at S$0.80 per unit. The placement tranche comprises 143.169m units with the retail tranche making up the balance of 8m units. The gross proceeds raised will be around S$394.2m. |

Principal business

As the name implies, BHG is a REIT focused (initially) on quality properties in Tier 1 and Tier 2 cities in China. Since investors in Singapore are very familiar with REITs, after providing some basic information, I will jump straight into what i think of BHG. Initial Portfolio

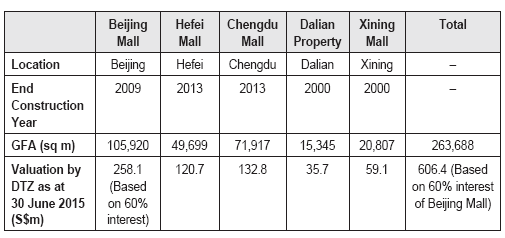

Initial Portfolio

The initial portfolio comprises of 5 properties listed below with valuations by DTZ and Knight Frank. It is good to see that the company is valuing it at >$$30m below the market value.

Valuation of IPO Properties

It is good to note that they are not pricing the IPO at the maximum valuation.

Forecast

The forecast below for record purpose.

Yield

The distributions will be made semi-annually.

The projected yield for FY2016 is around 6.3% but that is because strategic investors have waived their entitlements. The yield would drop to 4.5% if there had been no financial engineering! (I don't like it!) This financial engineering will be in place all the way till 2021!

|

What I like about BHG » China will be the biggest consumer market by 2018 and with rising income and middle class, consumer expenditure will drive the China economy. The relaxing of the one child policy is also positive for this sector » Changing consumer habits. With investors making purchases online via smartphones, a physical store may become obsolete over time and we can see that happening in China with rising online sales |

Peers

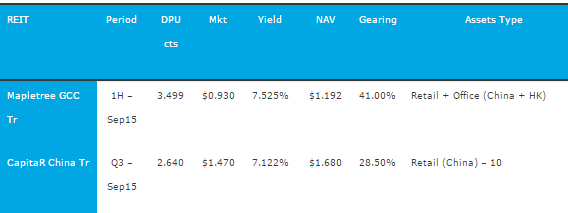

According to REIT data, Capital Retail China is trading at 7.122% with gearing of 28.5% while Mapletree Greater China Trust is yielding 7.52% with a 41% gearing.

In my view, the above two REITs provide better value propositions then BHG REIT in terms of dividend yield but definitely Capita Retail China Trust has a better debt ratio than Mapletree. Assuming BHG REIT trades to a yield of 7%, the fair value range will be between 51-72 cents

My chilli ratings

Considering this is the first mainboard IPO for Singapore Exchange for 2015, it is hugely disappointing. I will give it a zero chilli rating based on the above reasons.

Do note that i am vested as I have been allocated some shares in the placement tranche.

The article was originally published on http://singapore-ipos.blogspot.sg/ and is republished with permission.